It was September 1958 when Bank of America launched the first credit-card network with its BankAmericard. A month later, American Express launched the first worldwide credit-card network. Since then, consumers have seen a veritable arms race as credit card companies raced to build the biggest, most-reliable networks.

Today, so many credit card networks exist it begs a big question:

What credit card is the best?

That’s a tough question because there are so many ways to define “best.” Is it prestige? Domestic or worldwide acceptance of your card? Fringe benefits?

It all depends on what you want, personally, in a credit card.

That said, here are the differences to know about in choosing between American Express,

This article will cover

- What’s the Difference Between a Credit-Card Network and a Credit-Card Issuer?

- Which Credit Card Company is Bigger? And is “Bigger” Better?

- What Credit Card is Most Widely Accepted?

- How Much Do Merchants Pay to Accept a Credit Card?

- Is Credit Card Prestige a Factor?

- What Fringe Benefits Apply to Each Credit Card Brand?

- What’s the Best Credit Cards for Each Network?

What’s the Difference Between a Credit-Card Network and a Credit-Card Issuer?

First thing to know is that when you’re dealing with

When you apply for an Amex card, you are dealing with a company that both issue cards and run the network on which those cards are accepted. Basically, you’re dealing with American Express from the point of application to the point of sale to bill payment and customer service.

Honestly, it’s a distinction lost on most people, and in practical terms it doesn’t mean a whole lot to how you use your credit card. I tell you this just so that you understand there is an operational difference.

What you rightly want to know are those practical differences between the different credit-card brands before you go apply for one.

Which Credit Card Company is Bigger? And is “Bigger” Better?

Let’s answer the second question first: To a certain degree, bigger is better, at least in terms of a bigger network since it means more merchants accept your card (more on that in a moment).

As to which credit card company is bigger, that depends on how we slice the data.

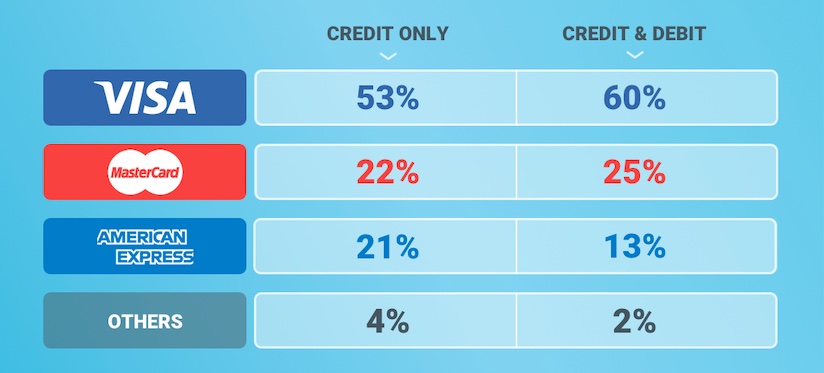

Visa is, by far, the biggest credit card network in terms of purchase volume, as you can see in this chart.

Data via nilsonreport.com

But in terms of purchase volume by credit card issuer, Amex is the Big Kahuna, followed closely by Chase’s parent, JPMorgan Chase. Citibank pulls into third place, with Bank of America and Capital One a good deal behind. (Chase, Citi, Bank of America and Capital One all issue both

So, if size is an issue, then focus on American Express, or a Visa/Mastercard issued by Chase, Citi, Bank of America or Capital One.

What Credit Card is Most Widely Accepted?

Merchant acceptance of a credit card is probably the biggest issue for most people. I cannot tell you how often I’ve pulled a credit card from my wallet and been told, “Sorry, we don’t accept that card.”

Generally speaking, you want a card that’s accepted at as many places as possible.

In global terms, Visa and Mastercard are, by a landslide, the most widely accepted cards on the planet with some 40 million merchants accepting each card. In the U.S. alone, nine million merchants accept

| Worldwide (million merchants) | U.S. (million merchants) |

|

|---|---|---|

| VISA | 40 M | 9 M |

| MasterCard | 40 M | 9 M |

| American Express | 25 M | 6M |

| Others | 42 M | 9 M |

American Express lags behind in the number of merchants who accept an Amex card. Globally, the number is estimated at 25 million merchants, while it’s around six million in the U.S. Still, in the U.S. just about every major merchant accepts Amex, and those that don’t tend to be smaller, local retailers and restaurants, or chains that have tied themselves to a specific credit card, such as Costco’s deal to only accept Visa cards.

Pro tip: When

If you’re only going to have one credit card, then clearly the advice is to go with Visa or Mastercard, since they’re accepted at a far larger collection of merchants.

How Much Do Merchants Pay to Accept a Credit Card?

Every time you use your credit card, you’re not the only one paying. The merchant pays, too.

With each charge, the credit card network imposes a fee on the merchant to process the transaction. The size of the fee depends on the network.

Mastercard generally charges between 1.55% and 2.6% for each transaction. Visa charges similar fees of 1.43% to 2.4%. And American Express charges the most: 2.5% to 3.5%.

In terms of picking the best credit card, this really isn’t much of a consideration, since it’s all back-office stuff you never need to think about.

However, it does have some practical impact on you, regardless of the credit card you choose. It explains why some merchants, particularly smaller

Is Credit Card Prestige a Factor?

That’s a personal determination, and some consumers really don’t care.

But, yes, there is a prestige factor with certain credit cards.

American Express is widely perceived as a more prestigious credit card. That could be a function of the fact that Amex has its normal green card, but also offers gold and platinum cards to certain consumers with a certain credit and income history. And then there’s the Amex Centurion card – the infamous “Amex Black” – a heavy, black metal card that’s offered only by invitation to consumers. (There are no published rules for obtaining an Amex Black, but the general consensus is that you must be high-net worth, with a high credit score, and spend at least $250,000 a year on another Amex.)

So, if prestige is a factor for you then aim for Amex, and, in particular, the Amex Platinum card (if you don’t mind the $550 annual fee). It’s the top of the heap until you qualify for Amex Black. The Amex Gold card is $250 a year.

If you just want a metal credit card, which is what the Amex Platinum and Gold cards are made from, then there are others now besides Amex. But be warned: Most have high annual fees, often in the $200 to $500 per year range.

Two

- Amazon Prime Rewards Visa Signature: 5%

cash back at Amazon and Whole Foods, 2% at restaurants, drug stores and gas stations , 1% everywhere else.

- Capital One VentureOne Rewards Credit Card: enjoy one-time bonus of 20,000 miles once you spend $1,000 on purchases within 3 months from account opening, equal to $200 in travel and earn 1.25 miles for every dollar you spend every day.

What Fringe Benefits Apply to Each Credit Card Brand?

This depends entire only the card.

Just about every card at any level comes with some degree of fringe benefits, whether it’s credit monitoring or rental-car insurance or free checked baggage when flying. Benefits vary greatly, so read through the benefits pages that every credit card issuer publishes online.

Some examples of what’s out there:

- Amex Platinum Delta SkyMiles offers a free round-trip companion ticket each year upon renewal of the card.

- Capital One Venture Card offers Travel Concierge Service, which is available 24/7 to make your wish a command, whether you have a travel emergency or want to find some last-minute tickets to a sold-out concert or basketball game.

- Chase United MileagePlus Club Mastercard: Free annual membership to United Airlines and Star Alliance airport lounges worldwide, as well as priority check-in and security lane access.

The point is, Visa, Mastercard and Amex cards offer lots of fringe benefit possibilities, depending on which version of the cards you research. Determining which card is better, therefore, depends on what benefits appeal most to you.

The Wrap Up

At the end of the day, the question of, “What’s the

I happen to frequently fly American Airlines (and the oneworld Alliance), and United Airlines (and the Star Alliance). For me, then, cards tied to those frequent flyer programs mean something tangible to my experience as a traveling writer.

Likewise, I like the

So, determine what matters most to your lifestyle and pick the card that best fits you. Or, do what lots of people do: Get the Amex you can afford, as well as a

And we want to know: What do you think defines the best credit card?

Leave us a comment below!