While Citi’s credit card application rules aren’t as complicated or restrictive as some issuers, they can still be confusing. It’s important to know these rules or else you risk being denied for a new card or forfeiting a sign-up bonus. In this post we‘ll cover the basics for applying and some strategies for insuring that you get the bonus.

Most of Citi’s rules are directed at individuals who have or are applying for multiple Citi cards. The bank is a major card issuer, so you may run into this situation more often than you’d think. For example, you can’t get both a Citi / AAdvantage Platinum Select card and a Citi Premier® Card in the same week because of Citi’s 8-day rule.

These are some of the more popular

| Citi Credit Cards | Annual Fee | Sign-Up Bonus |

|---|---|---|

| ThankYou Preferred (no longer available) | None | None |

| Citi Premier® Card | $95 | 60,000 ThankYou points |

| Citi Prestige® Card (no longer available) | $495 | 50,000 ThankYou points |

| Citi® / AAdvantage® Platinum Select® World Elite Matercard | $99 (waived for the first 12 months) | 50,000 AAdvantage miles |

| Citi® / AAdvantage Business™ World Elite Mastercard® | $99, waived for first 12 months | 65,000 AAdvantage miles |

| Citi® / AAdvantage® Executive World Elite Mastercard® | $595 | 70,000 AAdvantage miles |

| Citi Hilton HHonors Reserve (no longer available) | $95 | 2 free nights |

| Citi Hilton HHonors Visa Signature (no longer available) | None | 75,000 HHonors points |

How Many Cards Can You Have?

Unlike American Express, Citi does not limit the number of cards you can have. It does, though, place an overall

If a new card puts you over that credit limit, your application will typically go pending. Under these circumstances, call the Citi Reconsideration line at 1-800-695-5171 and ask the agent to move credit from an existing card to your new card.

The 8/65/95 Rule

While Citi doesn’t limit how many cards you can have, it does limit how often you can get a new card. The so-called 8/65/95 rule is shorthand for those restrictions and refers the number of days you have to wait before applying.

Officially, Citi says that you can get only one card a week and no more than two cards every two months. In reality, Citi has been known to deny customers who apply too soon. To be safe, you should wait at least eight and 65 days to avoid being denied.

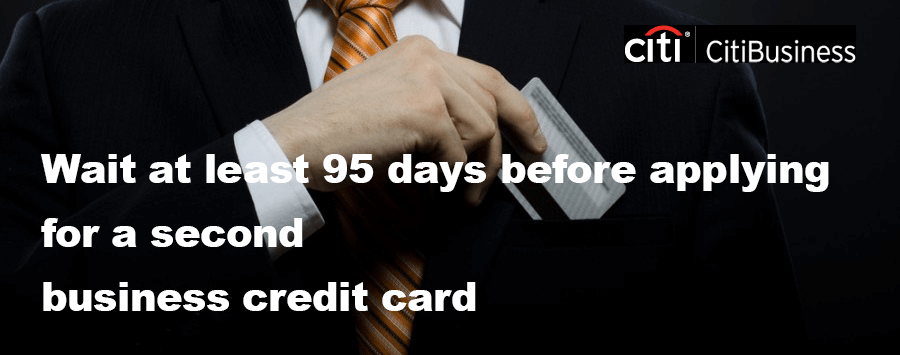

There’s an additional restriction for

It’s important to note that business cards also apply to the 8/65 portion of the rule. Under no circumstances can you get two cards in eight days or three cards in 65 days, even if one of them is a business card.

In other words, don’t apply for a new Citi card if any of these statements are true:

1. You’ve been approved for any Citi card in the last eight days.

2. You’ve been approved for any two Citi cards in the last 65 days.

3. You’re considering a Citi business card and you’ve been approved for a Citi business card in the last 95 days.

Unlike Chase, which has a similar 5/24 rule (only five new accounts in the last 24 months), Citi’s limits on new cards only apply to other Citi cards. Chase includes all new credit accounts when considering an application.

Getting the Sign-Up Bonus

Compared to its competition, Citi is generous with its

However, you can’t simply downgrade a card after

Call Before You Apply

Credit card rules can be confusing, and they can change without notice. On top of that, issuers will sometimes have different rules for different cards in their lineup. If you’re thinking about getting more than one Citi card, it’s worth the time to call customer service to be sure that you won’t run into any issues. Don’t risk being denied or missing out on a