You know the routine. You come home from work, and before heading inside you check the mail. Along with a bunch of coupons you’ll never use, you find a few bills and, yes, credit card offers.

The envelopes that the credit card offers arrive in are the result of a lot of science. The colors and even the texture of the envelope were created to send the message that you long to hear: you’ve been chosen.

There’s something in our brains that loves to hear messages of acceptance, and we’re all too eager to open the envelope, sign up and hopefully get that piece of plastic. It’s a good thing to be pre-approved before you apply, but don’t fall for the marketing tricks.

Be proactive. Find

What It Means to Be Pre-Approved for a Citi Credit Card

If you get a pre-approval offer from Citi in the mail, it doesn’t mean that you’ve been chosen to become a cardholder. Based on what the bank or credit card company believes to be true about you, that envelope is just an invitation to apply. Remember, though, that the simple act of applying could be detrimental to your credit.

Instead of just sending that application in and hoping you get that card, find out if you pre-qualify for the card you really want. If that credit card is from Citi, we can tell you how you can pre-qualify.

The Best Citi Credit Cards

Before we look at how the Citi pre-qualification process works, let’s look at some of Citi’s best credit cards. If you’re looking for a lot of options, you’ve come to the right place. Not only does Citi offer its own line of cards,

Below are our

The Best Cashback Card:

Citi Double Cash® Card

The Citi® Double Cash Card – 18 month BT offer card is one of the best cashback cards on the market. That’s because you’ll get a total of 2 percent cash back on every purchase. You’ll have to pay off your purchases to get the full reward, though, since the card offers 1 percent cash back when you purchase and 1 percent cash back when you pay.

To earn cash back, pay at least the minimum due on time. Plus, for a limited time, you can earn a bonus offer of $200 cash back after spending $1,500 on purchases in the first 6 months of account opening.

Excellent for Travelers:

Citi Premier® Card

The next step up from Citi’s basic line of cards is the Citi Premier® Card. It’s great for anyone who likes to travel because you can transfer your points to a variety of travel partners, including several frequent flyer programs. You can also purchase travel with your points directly through the Citi travel portal.

The ThankYou Premier card offers 3X points when you dine out at restaurants and shop at supermarkets. You’ll also get 60,000 points when you spend at least $4,000 within the first 3 months. Those points are redeemable for $600 in airfare on any airline with no blackout dates when you book through the ThankYou® Travel Center.

You’ll also get triple points on every dollar spent on air travel, including at gas stations and hotels. All other purchases will earn one point per dollar. While the card comes with a $95 annual fee, you can easily make that back if you take advantage of everything this card has to offer.

Pre-Approval by Citi and Soft Pulls

First, don’t get sucked in by Citi’s pre-approval hype. The envelope might say that you were pre-qualified and “0%” might be written in that gold colored ink to make it look even more glamorous. But Citi just did a soft pull on your credit to see if you qualify to receive the mailing.

Often a company will use a soft pull to see if you qualify for an offer. Or a potential employer might run a soft pull before making you a job offer.

These soft pulls don’t impact your credit score, but they also won’t qualify you for a loan, credit card or any other financial product. You have to agree to the next, more obtrusive step—the hard pull.

A hard pull is what a financial institution uses to make a credit decision about you. It’s an in-depth look at your credit score. By completing an application for a credit card, you’re giving the company permission to pull your credit and that can potentially have a negative effect on your credit score.

Don’t get too alarmed, though. A single hard pull isn’t going to ruin your credit score and a series of hard pulls in a close period of time for the same reason are often seen as one pull.

For example, when you’re shopping for mortgages, credit agencies understand that there might be multiple hard pulls. They know that they’re all for a single purpose and won’t ding your score.

Why You Should Pre-Qualify With Citi Before You Apply

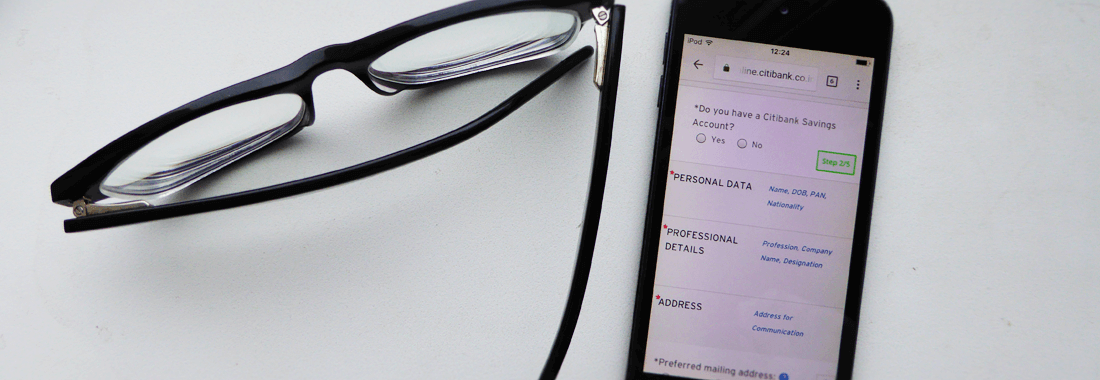

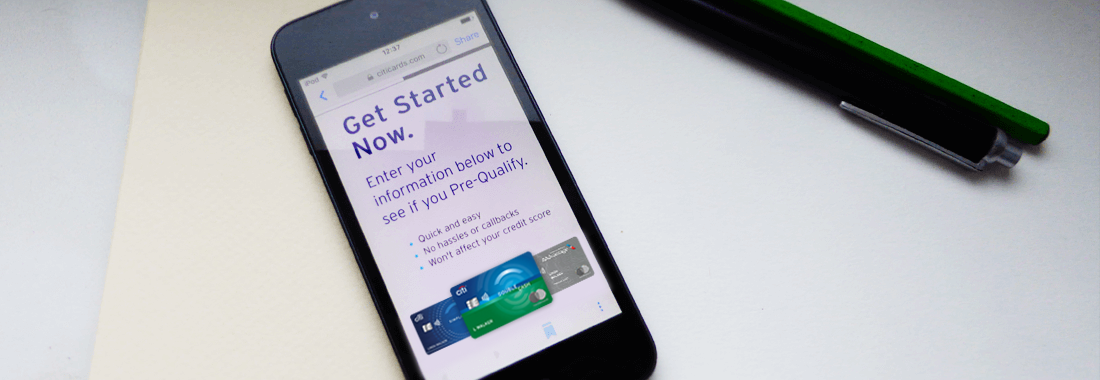

Before you actually apply for the Citi credit card you want, you should first see if you pre-qualify. Thankfully, that’s super easy to do. And since pre-qualifying is a soft pull, it won’t hurt your credit score.

You can use the online Citi pre-qualify tool to see which of its cards you’re pre-approved for. Simply complete the fields and Citi will give you a list of cards and a link to apply.

Remember that this pre-approval is only a soft pull and doesn’t guarantee that you’ll qualify for the card. It will, however, give you an idea of which of Citi’s cards you might be able to get. It’s a great way to improve your odds for approval and avoid an unnecessary hit to your credit score.

Even if you do qualify, your interest rate is also dependent on your credit score. If you later apply and get the card, pay careful attention to the rate. Even better, take the interest rate out of the picture by always paying the card in full at the end of the month.

Don’t Fall for the Pre-Approval Hype

Finally, a word of warning: credit card issuers spend a lot of money trying to figure out how to make you believe that you need the latest and

Credit card interest rates are much too high to hold a balance. Before looking for a

If you’re

Credit cards are tools. Like any tool, they can serve a positive purpose or be a vehicle for financial destruction. Don’t make decisions based on marketing hype. Make responsible financial decisions based on your current debt load, income

Remember, though, go to Citi’s website and get pre-approved before you apply. While it’s no guarantee, it can save you a hard pull on your credit by guiding you to the right card.