Have you tried applying for a credit card, only to be turned down time after time? Ever wonder why the banks keep telling you no? Want to know how you can change the response you get?

How to Get Approved for a Credit Card

Everyone knows that credit cards offer one of the easiest ways to establish a good credit history. If treated properly, that credit rating will last a lifetime. But getting approved for a credit card isn’t always as easy as it sounds.

If you have never had a credit card before or if you have a severely limited credit history, it can be difficult to find a bank that will give you a shot. And if you have already established a less than par credit history, the chances of being approved are likely worse.

While nobody can actually guarantee that you will be approved for a credit card, following these steps is a great way to improve your chances.

1. Check Your Credit Report

This should always be the first step when you are ready to apply for new credit. Your credit score is usually one of the biggest factors in determining whether you will be approved or denied. You can get your credit report for free from websites like freecreditreport.com.

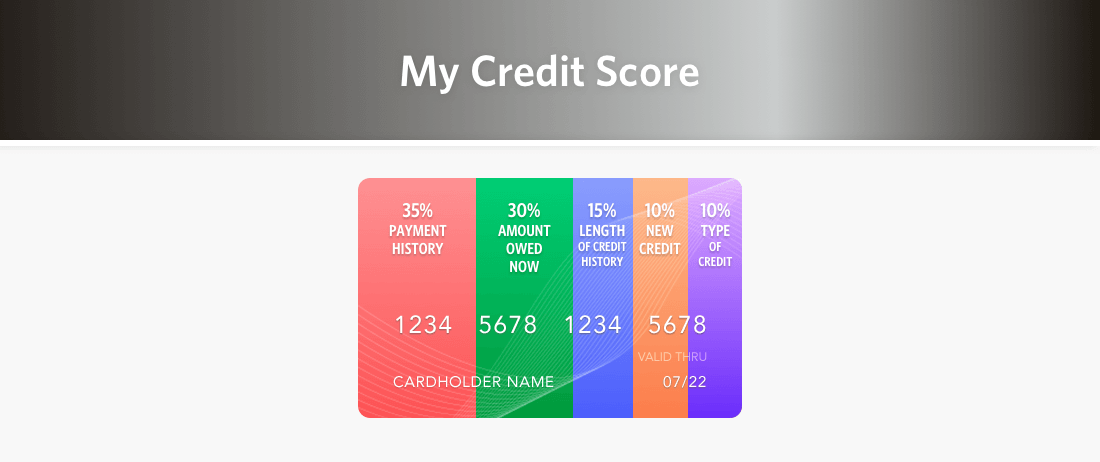

Your credit score is made up of several factors. Even if you’ve never had a credit card before, that doesn’t mean you don’t have a credit score. Items like student loans, car loans, and even utility bills can factor in to your credit score. Other important parts of your credit score include whether or not you make your payments on time, the amount of debt you have, how long you’ve had it, and how often you apply for new credit.

Knowing what kind of shape your credit is in will help you determine which cards you should be applying for and which will likely lead to an approval.

2. Search for the Right Credit Card Offer for Your Score

Once you know where you stand with your credit rating, you can start looking for a credit card offer that is appropriate for your credit status. You may be eager to apply for any offer you find, but it is best to put in some time to look for the right credit card offer for your situation.

Different credit cards offer different benefits and rewards, so it’s a good idea to be picky. For example, if you are trying to apply for a new card so that you can consolidate debt, you will want to look for one that offers a 0% APR on balance transfers. If travel rewards are more what you had in mind, then you will want to find a card that offers a generous sign up bonus and that accumulates points rapidly.

Of course, the higher your credit score, the more choosy you can afford to be. If your credit score is on the lower end of the spectrum however, your choices may be more limited.

3. Check Offers for Pre-Screening

One of the best ways to get approved for a credit card is to take advantage of pre-screened offers that you may receive in the mail. Instead of tossing them aside or in the trash, take a look at what these offers have to say. Your chances of being approved for an offer increase with these pre-screened letters from the bank. This is especially true if it is an exclusive offer with an invitation number on it. These special offers may be the closest thing to a guaranteed approval you will find.

4. Make All of Your Monthly Payments on Time

Sometimes improving your credit score is necessary before you can realistically apply for a credit card. One habit that is necessary both to get good credit and to keep it, is to pay your monthly bills on time. This includes utility bills, your cell phone, student loans, and any vehicle loans you may have. This is especially critical since your payment history makes up the largest portion (35%) of your overall credit score.

5. Pay Down Debt First

In addition to paying your bills on time, try paying down the amount of overall debt you have. The second biggest contributing factor (30%) to your credit score is your debt-to-credit ratio. Most banks don’t want to see someone who has $10,000 available to them in credit card debt, carry a $9,950 balance on those cards. The lower the balance is that you actually owe on any outstanding debt, the better your score will be.

6. Report All Income

When filling out a credit card application, it is easy to overlook some less common forms of income. If you earn any money outside of your regular job, be sure to include this amount on your application. You can also include any amounts you may receive in monthly alimony or child support payments. Another form of income that should be included is any government payments such as Social Security, or retirement or pension benefits.

Your total income is important to creditors so that they can figure your overall ability to make payments. The higher your income is, the more credit you will likely qualify for.

7. Use Prequalification Tools

Many banks offer tools on their websites that will tell you if you pre-qualify for one or more of their credit cards. Using free tools like this will keep you from applying for cards that you certainly have no chance at being approved for. These tools also do not have any negative impact on your credit score since they do not do a hard inquiry on your credit report.

8. Apply for a Secured Credit Card

When traditional credit cards fail, you can always apply for a secured card. These cards are a great way to at least get your credit moving in the right direction, especially if you are trying to establish credit for the first time.

Here are some great secured credit cards for you to consider:

Oftentimes a secured card will give you an initial credit limit after making a security deposit of a certain amount, determined based on your creditworthiness. Once you begin to establish responsible spending habits and demonstrate that you pay your bill each month on time, the bank will likely upgrade your account to an unsecured card and you will get your deposit back.

9. If Denied, Ask for Reconsideration

Did you know there is a department that is dedicated to reconsidering your denied application if you ask them to? It’s true! If you feel you have done everything right and your credit score is worthy of a credit card but you are still denied, you can call the reconsideration line to plead your case. Be sure you have checked your credit report recently so you aren’t surprised by anything they might be basing their decision on.

10. Be Prepared for a Long Journey

Sometimes getting approved for a credit card is not a simple matter. It would be great if we could all apply for whatever card we wanted and be approved instantly, but that simply is not the case for those who have a poor or limited credit history. It may take quite some time and a bit of effort to improve your credit worthiness before a bank is willing to take a chance on you. Be prepared for the long run.

The Bottom Line

Whether you are trying to apply for additional lines of credit or establish credit for the first time, it is never too soon to make good decisions when it comes to financial matters. Paying your bills on time each month and keeping your overall debt as low as possible will help keep your credit score on the healthy side, and improve any future opportunities for getting the credit card you really want.

The sooner you start making positive spending habits, the sooner you will be able to pick and chose which offer you want, rather than be stuck with few choices. The most important thing to remember is that having good credit is not something you should just get once, it is something you should strive to keep long into the future.