Credit cards should not be viewed as a way to access cold hard cash like an ATM. The goal of a credit card is as follows: a bank issues you a line of credit (also known as the card’s credit limit) and you are allowed to use the card to finance various expenditures up to the credit limit. You must pay back all of your expenditures in full on a due date set by the credit card issuer.

The Problem With Using a Credit Card to Withdraw Cash

If you fail to pay this balance or only make the credit card’s minimum payment, which is only a tiny fraction of what you owe, interest charges will accrue. With a credit card, you are using someone else’s money (the bank’s) to make expenditures. A cash advance is a very different situation than the traditional use of a credit card that we just outlined above. Let’s explore the ins and outs of cash advances and why they are a very expensive option.

With a cash advance, you’re not using the card to make various purchases like groceries, the cable bill or an airline ticket. A cash advance allows you to turn part of your credit limit into cold hard cash. You’re essentially tapping your credit card for cash just as you would at an ATM.

Just like using the credit card for purchases at a store is using someone else’s money, tapping your credit card for cash is also using someone else’s money. That “someone else” is the bank or credit card company. All cash advances must be paid back with interest.

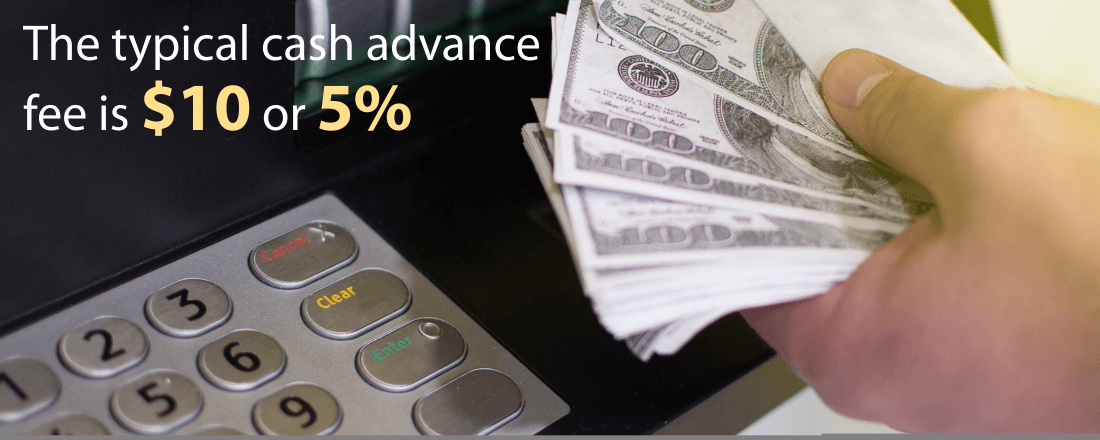

Credit Card Cash Withdrawals Come With High Fees

Cash advances are very expensive. The typical fee for a cash advance is $10 or 5% of the cash advance amount. The greater of these two amounts will be applied. If your cash advance is $1,000, you’ll pay a fee of $50. But if the cash advance is only $75, you’ll pay a fee of $10 — because 5% of $75 is only $3.75, which is lower than the $10 flat fee.

Keep in mind, this is just a fee for the cash advance. We haven’t even outlined the extra interest expenses that accompany a cash advance. The upfront fees are just a small part of the total expense of tapping your credit card for cash.

Cash Advances Come With Plenty of Interest Charges

As mentioned above, when using your credit card in the traditional sense for various purchases like groceries, gasoline or clothing, that balance must be paid back in full. The same line of thinking applies to credit card cash advances. That amount must be paid back.

The issue with cash advances is that the interest rate is significantly higher than the rate that applies to a credit card balance. On your credit card prospectus, the interest rate for a credit card balance and the interest rate for a cash advance will be clearly outlined.

You can also call the credit card company to retrieve this information. The typical interest rate on a credit card balance can be as high as 15%. The interest rate on cash advances could be ten percentage points higher than that. This means paying back a cash advance is much more expensive than paying back a traditional credit card balance.

How Cash Advances Affect Your Credit Score

A cash advance can harm your credit score, especially if you already have existing credit card debt. The way credit card debt affects your credit score is by raising your utilization ratio, which accounts for 30% of your credit score. The utilization ratio is a measure of how much you owe across all the different credit cards you have vs. the available credit limits you have access to.

If you owe $2,000 on a credit card that has a credit limit of $5,000, your utilization ratio is 40%, which is rather high (2,000 divided by 5,000 * 100). If you then take out a $300 cash advance, your owed balance will rise to $2,300 (2,000 + 300). That means your utilization ratio is now 46% (2,300 divided by 5,000 * 100). The higher utilization ratio will ding your credit score.

Remember, a high credit score is critical if you are in the market for a mortgage, car loan or any other type of loan. With a high credit score, not only will it increase your chances of being approved for the loan, but it will also result in a lower interest rate on that loan. A lower interest rate means lower monthly payments. On the flip side, a lower credit score will result in a higher interest rate on the loan. That means higher monthly payments for you and a more difficult journey of eventually becoming debt-free.

When Withdrawing Cash from a Credit Card Cash is Okay

There are certain circumstances when a cash advance can be a reasonable option if you find yourself in a very short-term cash squeeze. Let’s say your rent payment is due at the end of a given month and the landlord only accepts the rent via cash and not a credit card. But your next paycheck from your job doesn’t arrive until the very beginning of the following month. And you need that paycheck to make the rent payment that’s due at the end of the current month. You are now in a 24-72 hour cash squeeze.

Even once you receive that paycheck, it could take 24 hours for the money to clear in your checking account. A cash advance can help you in this situation. It will allow you to make your rent payment on time and you can then pay back the cash advance as soon as you receive that paycheck. This will result in only a few days of interest. Cash advances can be a viable option if you are able to repay them within a few days. The longer you wait, the more interest you’ll end up paying.