Everyone tells you that you need a good credit score. But how many of those people can actually tell you how to build credit? This comprehensive guide will show you the best way to build credit and improve your credit score. No matter if you’re a seasoned pro or are just starting out, we have actionable tips for you that will show you how to build credit fast and improve your credit score.

This article will cover

- How to Build Credit with a Credit Card

- Best Credit Cards to Build Credit

- What to Look for When Picking out a Credit Card

- How to Build Credit without a Credit Card

- How to Improve Your Credit Score

- What is a Credit Report?

- How do Credit Scores Work?

- How to Build Credit Responsibly

- What Can a Great Credit Score Do for You?

How to Build Credit with a Credit Card

So, how to start building credit? In my opinion, the best way to build credit is with a credit card. Credit cards can be easy to get approved for because there are so many options. It is the fastest way to build credit. Don’t worry, we’ll walk you through the best credit cards options to build credit below.

Not only are credit cards my favorite way how to build credit fast, but they also have the biggest impact on your credit score. That’s why I start by teaching people how to build credit with a credit card first.

Banks that issue credit cards report your account details every month to the three credit reporting agencies. When you make your payments on time and stay within your credit limit, that positive behavior is reported each month. If you pay late or go over your limit, that negative information is also reported.

When applying for credit, banks like to see that other banks trust you and that you’ve handled your existing accounts responsibly. This gives them more confidence in approving your credit request. This built-up trust with one bank is the best way how to establish credit with other banks.

Be careful when applying for credit. Too much of a good thing can be bad. When banks see someone have numerous credit applications in a short period of time, that makes them think that the person is in financial trouble. This is not how to build credit fast!

Each credit application results in a hard inquiry into your credit history. And every credit inquiry can reduce your credit score by 3 to 5 points. For more information about how many credit cards should you have, read this article.

By using a credit card responsibly and only applying for new credit when needed, the positive payment history, longevity of your account, and low credit utilization all work to improve your credit score.

Best Credit Cards to Build Credit

But which credit cards offer the best way to build credit? There are literally thousands of credit cards to choose from. We have narrowed down the best credit cards based on the category that fits the FICO credit score range of your profile. If you have questions about which credit card is best for you, you can always contact us for personalized credit cards recommendations.

Secured Credit Cards

Almost everyone can get approved for secured credit cards because the bank’s risk is limited to the deposit you’ve already made. Secured credit cards are the fastest way to build credit for people rebuilding their credit report. Some secured credit cards will increase your credit limit after making several payments on time. And others offer the ability to convert to an unsecured credit card once you’ve shown the ability to handle the secured credit card responsibly. When your secured credit card is converted to an unsecured credit card, you’ll get your deposit back.

Before applying for a secured credit card, make sure that the credit card issuer will report your responsible credit card use to all three credit bureaus.

Student Credit Cards

Students always want to know how to start building credit. They are just starting out in life and have freedom that they never had as a child. But now they also have the responsibilities of being an adult. The right credit card is the fastest way to build credit for students.

Banks love students. They know that student are going to college to improve your life and grow your income by getting a degree. Banks want to develop a relationship with you while you are young and mold you into a lifelong customer. Ideally, you will use their credit cards, apply for their home and auto loans, and open up bank accounts with their bank.

Because most students are young, due to federal law, they must provide proof that they can repay the debt. Alternatively, the student can have a co-signer (like a parent or other trusted adult) who will also be responsible for paying the credit card. Any good behavior, or bad, will report on both people’s credit reports.

Store Cards

Store cards are similar to credit cards, but there is one big difference. Unlike Visa, Mastercard, Discover, and American Express, store cards can only be used at the store (or family of stores) that is named on the card.

If the store cards are limited to one store, is this really how to establish credit? Yes, it is! Just like a credit card, store cards help build your credit. The bank that issues the store card will report your payment history, credit limit, and the balance owed each month to the three major credit bureaus.

Once approved, you receive a credit limit and are able to make purchases with it. You will have a minimum payment due each month and, if you don’t pay the balance in full each month, you will be charged interest on the unpaid balance.

One thing that is nice is that some store cards offer promotions only available to cardholders. For example, my Lowe’s store card offers a 5% discount or 6- to 18-months 0% financing on purchases. And my Kohl’s store card gives a larger discount than what is available when paying with a traditional credit card, cash, or a gift card.

Improve Credit Score with the Shopping Cart Trick

If you are having trouble getting approved for a store credit card, you should read about the “shopping card trick.” This little-known hack is a way to get a pre-approved or pre-qualified credit card offer from some online retailers.

Read the article for full details and a list of some retailers that participate in this strategy. To summarize the shopping cart trick, when pretending to make a purchase, some retailers will offer you a pre-qualified credit card from their store right before you check out.

When you see the offer presented, apply for their store card and the chances are really good that you’ll get approved. Then go back to the shopping cart and cancel the rest of the transaction.

Upgrading from a Secured Credit Card Automatically

When you have a secured credit card, the banks will review your account on a regular basis. They are checking on your to make sure that you handle your secured credit card responsibly. Your continued responsibility is one of the most critical lessons in how to establish credit. Some are reviewing your activity to see if you qualify for an upgrade to an unsecured credit card. Here’s how the process goes:

- The bank will review your account to ensure you’re making your payments on time and using only a portion of your available credit. The review process varies by credit card issuer, but it usually begins 8 to 18 months after your account opened.

- Upon approval to upgrade from a secured card to an

unsecured credit card, you will receive your security deposit back. With some banks, your security deposit earned interest while it was on deposit.

- You will receive an unsecured credit card. In most cases, the credit card number will not change, only the design on the card. You can continue to use your old secured credit card until the new unsecured credit card arrives in the mail.

What to Do if You’re not Automatically Upgraded from a Secured Card

If you’ve been handling your secured credit card responsibly and have not been upgraded after 18 months, it is time to be proactive.

- Go online and check your credit score to track your progress. Here’s how to get your credit score free from all three credit bureaus. If your score has not been improving over the last year and a half, what has been going on? You may need to speak with a credit professional to help you review your credit reports and develop a personalized strategy. Before your meeting, download your free credit reports from AnnualCreditReport.com.

- Contact your bank to ask them if you qualify for an upgrade from a

secured credit card to anunsecured credit card. - If your bank says no, it may be time to search for a new credit card that fits your credit experience. Since you’ve been handling your credit responsibly for the last 18 months, there are banks that will reward that positive behavior.

- Check for pre-qualification for credit card offers. This in-depth guide will show you how to check for pre-qualified credit card offers from every major bank. Don’t worry, searching for pre-qualified credit card offers will not affect your credit report because they are “soft inquiries.”

If you want to know how to build credit fast, one of the best banks to work with is Capital One. They are one of my favorite banks if you want to learn how to build credit with a credit card. Read this step-by-step tutorial to learn how to pre-qualify for Capital One credit cards.

What to Look for When Picking out a Credit Card

When learning to how to build credit with a credit card, it is important to know that you can’t just pick any credit card. Some credit cards have annual fees and high interest rates that you need to watch out for.

Is it Ok to Pay an Annual Fee?

Many people

When you’re first starting out, I would avoid credit cards with an annual fee. Most likely you are not getting enough benefits to justify paying extra money. An annual fee for credit cards will vary, but many are around $100 per year.

As you learn how to build your credit with credit cards and improve your credit score, then you can graduate to credit cards with an annual fee. These cards may provide

What is the Interest Rate?

Interest rates on unsecured credit cards and secured credit cards are important. But they shouldn’t be. We don’t want you to pay the banks any more than you have to.

Strive for a

If you need help paying off your debt, read this in-depth guide showcasing several debt payoff strategies that are proven to work.

What FICO Score is Needed?

Every credit card is designed for a certain FICO score range. Premium credit cards, like the Chase Sapphire Reserve, are designed for people who have a high FICO score and are willing to pay a high annual fee.

You can improve your FICO score and get into the right credit score range by following these steps. Get your FICO score from all three credit bureaus to know what your starting point is. Review your free credit reports from all three credit reporting agencies from AnnualCreditReport.com. Fix any errors you find. And follow these tips how to improve your credit score quickly.

Secured Credit Card vs. Unsecured Credit Card

By knowing your FICO credit score, you can review credit card details to see if you fall in the right credit score range to get approved for an unsecured credit card. A good way to do this is to look for pre-qualified credit card offers. An unsecured credit card is one that a bank will issue without requiring a security deposit based on your positive credit history.

A

Obviously, the preferred choice is to get an unsecured credit card. But there is no shame in needing to start out with a secured credit card. We all have to start somewhere. In fact, I had a couple of secured credit cards when I was in college as I was building my credit history.

How to Build Credit Without a Credit Card

I believe that the best way to build credit is by using a credit card. But that is not the only way. Banks like to see a mix of credit on your credit report and taking out a loan is another way how to establish credit. Pay a loan every month on time is a great way to show that you can handle this type of debt.

Apply for a Credit Builder Loan to Improve Credit Score

For borrowers that are having difficulty getting approved for other loans, a credit builder loan might be the best way to build credit. It can also be the fastest way to build credit because you are guaranteed approval. These are not the typical loans that you are accustomed to.

In basic terms, you make monthly payments to a bank that gets deposited into a savings account. Once you have reached the savings goal, the bank will return the money to you. The bank reports your on-time payments to all three credit reporting agencies and charges a fee for handling the payments, preparing statements, and reporting your history to the bureaus.

Mortgages

If you are having a hard time getting approved for a loan or credit card, I don’t think you should commit to a mortgage. But, we all need a place to live. And, if you’re going to pay rent to a landlord, for some people, you could be better off making a mortgage payment to the bank.

Mortgages help balance out your credit profile by showing a long-term loan with a track record of on-time payments with the credit reporting agencies. And, if you buy the home at the right time in the right location, the home could also appreciate in value.

Auto Loans

Taking out an auto loan can also help your credit. Just like a mortgage, the auto loan will show other banks that you are trustworthy and can make consistent on-time payments.

Before heading to the dealership, contact your local credit unions to get pre-approved for an auto loan. You’ll often get better terms and can negotiate from a position of power knowing that you don’t need the auto dealer’s financing to be able to buy the car.

Personal Loans

Many banks and credit unions offer personal loans. These loans are unsecured and can carry a higher interest rate. My suggestion would be to take out a small loan, make a few normal on-time payments, then pay it off as quickly as possible.

Remember, your credit score is not based on the dollar amount of the loan you borrowed. It is based on you making the payments on time.

Take out a Federal Student Loan

Taking out a federal student loan has a couple of advantages. First, it will help you build credit with on-time payments reported to the credit reporting agencies. Second, going to college and getting a degree is a great way to build your career and make more money.

You do not need good credit to get approved for a federal student loan. Simply complete the Free Application for Federal Student Aid (FAFSA) and you will get a loan to pay some or all of your classes.

Just like any loan, do not borrow more than you feel comfortable being able to pay back. Student loans cannot be discharged in bankruptcy except in extreme cases. So, you will have to pay back these loans.

On the positive side, student loans are an installment loan and are reported to the credit bureaus. They are one of many ways how to build credit without a credit card.

Peer-to-Peer Lending

On peer-to-peer lending websites such as Lending Club and Prosper, borrowers can apply for loans that are funded by people rather than banks. The people who lend money are investors who are looking for better rates of return than what a bank will provide them. These investors diversify their investments by placing their money into many different loans to borrowers like you. When you take out a peer-to-peer loan, you will be borrowing from multiple investors but making only one payment.

Most peer-to-peer lending platforms report your payment history and loan details to the credit reporting agencies to build your credit history. But confirm that this is the case before you complete your application.

Interest rates on peer-to-peer loans are often lower than what you’d receive from a bank. Additionally, there is often less paperwork involved during the application process.

Find a Co-Signer

If your credit profile is not strong enough to get approved on your own, adding someone with a strong profile as a co-signer could get you approved. Adding a co-signer is common with student credit cards because most college students do not have enough income to qualify on their own.

Be careful with any account in which you have a co-signer. Not only could any mistake affect your credit, but it can also impact your co-signer’s credit score as well. Many co-signers request a copy of the statement and notification when payments are made so that they can keep track of the account. They don’t want to make the payment on your behalf, but many people will do it to save their credit score.

Become an Authorized User

Becoming an authorized user is the flip side of adding a co-signer. Instead of adding a strong credit profile to your application, you are being added to someone’s existing account. It is the fastest way to get credit because you aren’t actually applying for credit. You are just being added to an existing account with a strong credit history.

When someone adds you as an authorized user on their account, they are trusting you with access to some, or all, of their credit limit on that account. Don’t betray that trust by spending more than you can pay off in full each month.

Keep in mind that any mistakes that the primary cardholder makes with their account will affect you as well. Most borrowers with a strong credit profile are responsible, but bad things can happen to good people.

Request Rent, Utilities, and Others to be Reported

Most landlords, utilities, and other normal bills are not reported to the credit bureaus unless you haven’t paid. However, in some cases, you can request that they report your positive payment history to the credit reporting agencies to help improve your credit score.

This is an excellent way to build credit history without applying for any additional debt.

Contact these businesses and ask them what options you may have. The worst that they can say is “no, we don’t have the ability to do that.”

How to Improve Your Credit Score

Not only do we want to help you learn how to build credit, but we also want improve your credit score. The good thing is that many steps in the process are the same. However, if you already have a credit history, pay attention to these steps so you can protect your credit score.

Fix Errors on Your Credit Report

According to a study by the Federal Trade Commission, 26% of participants had at least one error on their credit report. The federal government passed a law requiring all three credit bureaus to provide one credit report each to every U.S. citizen each year.

If you have errors on your credit report, this is the fastest way to build credit because errors can impact your credit score so much.

Get your free credit reports from each credit bureau each year from the government-mandated website AnnualCreditReport.com. You can receive all three at once, or you can space them out throughout the year. If you have the time and are willing to put in the effort, I’d say do them all at once and get it handled. For people stressed for time, choose one now, then review and fix any errors. Move on to the next and repeat the process until you’ve reviewed all three credit bureau reports.

If you find an error, you can dispute the error online through that credit bureau’s website. The process is very easy, however, each credit bureau has a slightly different process. In general, select the item that has an error, state why it is an error, then wait for them to research it. It could take up to 30 days to receive a response either by mail or through their online portal.

Protect Your Credit Score

You need to protect your credit score like it is a sack of money. Having a good credit score can literally save you thousands on your next car loan or mortgage. And people with great credit can

Some of my favorites include the Capital One Savor (4% cash back on dining and entertainment) and Capital One Venture (2% on everything with no travel blackout dates). The cash back earned can either be used as a statement credit to offset your next bill or you can request a transfer to your bank account.

With the law that went into effect in September 2018, borrowers can freeze their credit reports for free. This keeps any hackers and fraudsters from successfully applying for credit in your name. And when you’re ready to apply for a credit card or any other loan, the credit bureaus must unlock your credit report within one hour of your request.

What is a Credit Report?

A credit report is a biography of your borrowing history. The report will show your current accounts, accounts that you have paid off or closed, and any hard inquiries you’ve made in the past two years. Information related to charge-offs, collections, liens, judgments, and bankruptcy will also be reported here, if applicable.

Each of the three major credit bureaus – Equifax, Experian, and Transunion – collect and report this information. However, not all three credit reports will look the same because not every bank or other company reports to all three credit bureaus.

Understanding Your Credit Report

Looking at a credit report that is several pages long and filled with strange numbers can be overwhelming. Take a deep breath and short pause, then dig in and you’ll realize it isn’t that bad once you get used to the format.

There is a section of your personal information. Your current and former addresses. Current and previous employers. And your Social Security Number.

The section with all of your open and closed credit accounts could be short or long, depending upon your credit experience. Each account looks very similar. It shows the name of the lender and your account number. The latest balance and credit limit are listed, as well as the minimum payment due on the account. A history of payments shows whether you paid on time or were late. And, if you were late, it will say 30, 60, or 90 days late.

Don’t worry. If you paid your credit card or loan late by a few days, you may be charged a late fee, but it won’t show up on your credit report. A late payment on your credit card means that you were late at least 30 days from the due date.

Any hard credit inquiries will also show. These hard inquiries stay on your credit report for two years, but only impact your credit score for 6 to 12 months. Most banks will pull from one credit bureau and not the others. This contributes to why each credit report and credit score from the three credit bureaus will differ.

How do Credit Scores Work?

Credit scores are calculated based on the information that banks and other agencies report to the credit bureaus. A credit score is often thought of as a fixed number, but that is completely wrong. Credit scores are more like living, breathing animals.

Your credit score could be one number today and a different number tomorrow if one of your accounts provided updated information.

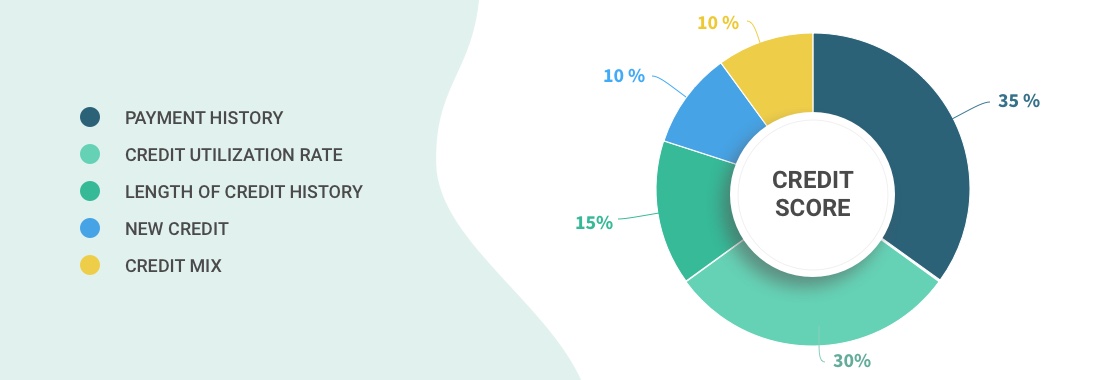

Many factors go into a credit score. Your history of payments is the biggest factor at 35%. How much of your credit limits are being used is 30%. The length of your credit history is 15%. And the mix of credit and new inquiries are 10% each.

Credit scores are calculated by either FICO and VantageScore. Every bank has a preferred provider. Click here to read how to get your free credit score from all three credit bureaus.

How to Build Credit Responsibly

I know you want to learn how to build credit fast, but we have to be responsible about it. These strategies showcase the best way to build credit responsibly. You have to remember that this is a marathon, not a sprint.

If you do this correctly, you will have amazing credit scores for the rest of your life. If you skip a step or do something wrong, your credit report could be hurt for many years. Possibly even for the next ten years!

You want to learn how to build your credit and do the following:

- Start slow and don’t rush it

- Use beginner credit cards as stepping stones to better cards

- Make all payments on time

- Don’t charge more than you can pay off each month

- Use less than 30% of your credit limit

- Apply for credit only when necessary

For example, I set up automatic payment of my credit card minimum payment from my checking account. This keeps my account current and avoids late charges.

These simple steps are the best way to build credit. They will improve your credit score and help you achieve your goals.

What can a great credit score do for you?

A world of opportunity is open to you when you have good credit. That is why it is so important to learn how to build credit and improve your credit score. It is important to learn

Now that we know how to start building credit, what have you done to improve your credit score?

Are there any mistakes that you’ve made that other readers should avoid?

Let us know in the comment section below.