One of the main things that keeps people from taking advantage of the myriad generous reward credit card bonus offers out there is the fear that applying for credit cards will have a negative impact on their credit score.

But that fear is usually not based on an actual understanding of how a credit score works and how new applications affect it.

So let’s yank the door open on that boogie man in the closet and take a good, hard look in the light of day.

What Goes Into Your Credit Score?

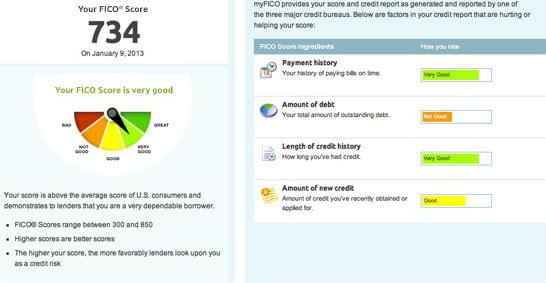

Credit scores, also called FICO scores for the Fair Isaac Corporation that created the grading system, provide potential lenders a quick snapshot of your credit history.

Like an SAT score in college applications, the FICO score doesn’t necessarily make or break your application on its own, but rather provides a general starting point or guideline for determining whether you are a good fit for the type of credit you’re applying for.

Five main factors, each with its own level of influence, go into your credit score:

| Payment history | Amount owed | Length of credit history | Types of credit used | New credit |

|---|---|---|---|---|

| 35% | 30% | 15% | 10% | 10% |

The Real Truth: How Credit Card Applications Impact Your Credit–or Not

As you can see, there is only one area of your credit score and history that applying for new credit (whether a loan or a credit card) actually touches: the last piece of the pie, which makes up just 10 percent of your credit score.

Since it is such a small portion of your score, you don’t usually have to worry about one or two (or even three or four) credit card applications causing your credit score to take a dive.

{kind=link}

The one thing to watch out for is having too many applications in a short time that don’t all go through.

The new credit section of your credit score is meant to alert lenders about your applications for new credit so they can decide if it looks like you are applying for more credit in a healthy way or in a way that will make it difficult for you to meet all the obligations of your new applications.

Having several credit applications at once that are all approved for a substantial credit increase shows that other lenders have faith in you. But if you have several new applications that are denied, or perhaps approved for very little credit, it sends a signal to potential lenders that your other new possible lenders are wary of you.

This doesn’t mean that you can’t or shouldn’t apply for multiple cards at once. But if you are doing so, you have an extra duty to your credit score to call the reconsideration line if you get a denial or a low credit line. More on that later.

New Applications Can Make Your Score Go Up!

One of the things that people who don’t have very many credit cards often notice when they first dip their toe in the reward card water is that adding one or more new credit cards can actually make your credit score go up. Sometimes dramatically.

This is a function of section two of the credit score puzzle: amounts owed vs. credit available, which is also often known as credit usage or debt-to-credit ratio.

If you only have one or a couple of credit cards that you got when you were young, you may have a very low total amount of credit available in general on each card, often around $2,000-$3,000.

After developing a good credit history, you can often easily get a new card with a credit line of $10,000-$15,000, which provides a high bump to your available credit.

The more available credit you have, the more trust lenders have in you, increasing your credit score.