Who says you can’t get something for nothing? There are number of

No-fee cards aren’t all the same, though. If you’re thinking about getting one, you should consider how you plan to use the card and what you want to do with your points or miles. And if this isn’t your first card, it’s important to think about which no-fee card will best compliment what’s already in your wallet.

These cards fall into three categories based on the flexibility they offer you for spending your points or miles.

The best cards offer you the option of transferring your points to frequent flyer programs. If you do that, you can get the most value for your points. Only one no-annual-fee card allows you to do that, the American Express EveryDay card.

There are a few others that allow you to redeem through their respective awards programs, but don’t allow you to transfer points. They include Chase Ink Cash Business, Chase Freedom, Chase Freedom Unlimited and Citi ThankYou Preferred.

It’s important to note that if you have another card in these programs, such as the Chase Sapphire or Citi ThankYou Premier, you can transfer points to airlines. That makes this category of cards excellent for boosting your points balance on a card you already own.

The final category of cards, including offerings from Capital One and Barclaycard, are not a part of a rewards program and do not offer airline transfers. They work like cash back cards, allowing you to redeem miles for statement credits to cover travel purchases.

Though there’s nothing wrong with this type of card, they aren’t as useful because you’ll never get the maximum value for your miles.

American Express EveryDay Card

This card gets its own section because, as far as I know, it’s one of a kind. It’s the only no-fee travel rewards card that allows you to transfer points to frequent flyer programs. You also get access to the American Express Rewards travel center, where you can purchase all or part of your flight or other travel expenses with points.

The card doesn’t come with a huge sign-up bonus, but it does have one. You get 10,000 points after spending $1,000 in the first three months of having the card. You also get double points on groceries, something you’re likely to buy regularly. You can earn the bonus points on up to $6,000 of groceries a year. After that, like all other purchases, you’ll earn one point per dollar.

If you make 20 purchases or more in a billing period, you’ll get 20 percent extra points.

The EveryDay card’s best feature, though its flexibility. As part of the Ultimate Rewards program, you can transfer your points to 16 different frequent flyer programs. That’s more than ThankYou or Ultimate Rewards, which offer 12 and 6, respectively.

The program’s airline partners are good, too. They include Delta, British Airways, ANA and Air France, as well as budget carriers, like JetBlue and Virgin America, and luxury airlines, such as Emirates and Singapore Airlines.

Though this card doesn’t have a lot to offer if you already have an Amex Membership Rewards card, you might consider it if you have the Green or Premier Rewards Gold cardcard since it’ll give you an additional double-point earning category and a quick 10,000-point boost.

Chase Ultimate Rewards Cards

Chase offers three no-fee cards that give you access to its Ultimate Rewards program. The Freedom and Freedom Unlimited are personal cards, and Ink Cash is a business card.

| Chase Freedom | Chase Freedom Unlimited | Chase Ink Cash Business | |

|---|---|---|---|

| Sign-Up Bonus | 15,000 points | 15,000 points | 20,000 points |

| Bonus Earning Categories | 5x in quarterly rotating categories | 1.5x all purchases | 5x for offices supplies, phones, internet and cable; 2x for gas and restaurants |

To get the most value for you points, you’ll want to be able to transfer them to airlines. In order to do that, you need to have one of Chase’s premium rewards cards, like Sapphire Preferred.

Sapphire is an excellent card that comes with a 50,000-point sign-up bonus and a 20 percent discount on travel purchased through the Ultimate Reward travel center. Perhaps best of all, though, is that its bonus earning categories dovetail nicely with Chase’s no-fee cards.

Chase’s offerings really excel when it comes to bonus earning categories. The Freedom card offers an impressive five points per dollar spent on rotating quarterly categories that may include gas, groceries, restaurants and a variety of other types of retailers.

You can earn the quintuple points on up to $1,500 of purchases per quarter. If you max that out, you’ll get 7,500 points per quarter, or 30,000 points a year. Not bad.

If you qualify for a business card, you should consider getting the Ink Cash card, too. It offers the same five points per dollar, but on office supplies, landlines, cell phones, internet and cable. Those recurring bills can add up fast, and the bonus earning is good for up to $25,000 in purchases a year. If you max that out, you’ll get a whopping 125,000 points.

The Ink Cash also offers double points for gas and dining out, making it a very impressive earner, particularly for a card without an annual fee.

While the Freedom Unlimited card doesn’t have any wow-inducing quintuple-earning categories, it does offer a nice 1.5 points per dollar spent on anything. This card is a good all-around earner, and a good option if you don’t think you’ll be able to take advantage of the bonus categories the other cards offer.

Now combine the Sapphire Preferred card, which earns double points on airfare and travel, with any of the no-fee Chase cards and you have fantastic earning potential and flexibility.

Citi ThankYou Cards

Like the no-fee Chase cards, the Citi ThankYou Preferred card does not allow you to transfer points to airlines unless you also have a premium card, like ThankYou Premier. You do, however, get access to the Citi ThankYou program.

As of writing, the ThankYou Preferred card does not come with a sign-up bonus. Without the sign-up bonus, I’m not sure the card’s worth getting. The good news is that Citi sometimes offers a 20,000- to 30,000-point bonus. It would probably be worth waiting for that offer to be available again.

The reason why I probably wouldn’t get this card without the sign-up bonus is because it doesn’t offer anything you wouldn’t already get with the ThankYou Premier card. And without the Premier card, you won’t get the maximum value for your points because you won’t be able to transfer them to airlines.

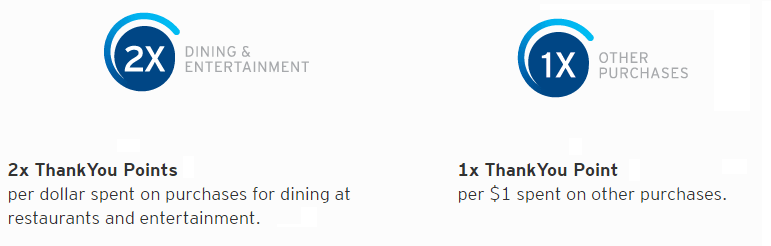

Both the Preferred and Premier cards offer two points per dollar for dining out and entertainment, but the Premier card also offers triple points for travel, including gas. Though it has a $95 annual fee, it’s a better earner that has a lot more flexibility in terms of spending points.

The only reason to get the Preferred card (without the bonus) is if you want to check out the ThankYou program without paying an annual fee.

Cash Back Travel Cards

Though this category of cards is of the least interest to me because you will never be able to transfer the miles you earn to a frequent flyer program, they might be useful to you if you’re just getting into travel rewards.

Two of these types of cards are the Capital One Venture One Rewards card and the Barclaycard Arrival World MasterCard. Both are solid no-fee cards that allow you to use miles for statement credits towards travel purchases.

| Capital One Venture | Barclaycard Arrival | |

|---|---|---|

| Sign-Up Bonus | 20,000 miles | 20,000 miles |

| Earning Potential | 1.25x all purchases | 2x for travel and dining; 1x all other purchases |

Both cards come with a decent 20,000-mile sign-up bonus and good earning potential. With the Capital One card, you’ll get 1.25 miles for every dollar you spend, and Barclaycard gives you double miles on travel and dining, and one point for everything else.

Which Card Should You Get?

If I was getting my first and only travel rewards card, I’d go with Amex EveryDay. It comes with a sign-up bonus and a decent earning scheme, offering double points on groceries. More importantly, though, it allows you to transfer your points to 16 different frequent flyer programs. None of the other cards allow you to do that.

On the other hand, if I already had the Chase Sapphire Preferred card, or if I was willing to pay the $95 annual fee, I’d get one or more of the no-fee Chase cards. Their phenomenal quintuple earning categories are hard to beat, and they really complement each other well, without much overlap from card to card.