We all end up with too many credit cards at some point.

You go to the department store or a specialty retailer and you’re making a big purchase, and if you sign up for their branded credit card at check out, the clerk lets you know, “you can save an additional 20% off your purchases today.” So, you sign up. Or you decide you want to start collecting

Maybe you want to cancel one or two … or five … but you remember hearing that maybe cancelling your credit card isn’t the best strategy, since it might impact your credit score. Besides, it’s good to have access to a lot of credit – right? Right?

Well, maybe. Then again, maybe not. So, here’s all you need to know to about credit card cancellation and how to cancel a credit card properly without hurting your credit score (too much).

This Article Will Cover

- First Question: Should I Cancel My Credit Card?

- Does Closing a Card Hurt Your Credit Score?

- What If I Just Want to Switch to a Better Credit Card?

- What If I Still Want to Cancel a Credit Card?

First Question: Should I Cancel my Credit Card?

That depends. Why do you want to close your credit card account?

Just because you’re not using a card doesn’t mean you should necessarily consider credit card cancellation as your only option. Credit scores depend, among other things, on the number of credit accounts you have, the age of those accounts, and the utilization rate of your credit (the size of your account balance relative to the total credit limit you have).

If you happen to close a credit card you’ve owned the longest and which has the highest credit line, you can be sure your credit score will suffer. That’s not a good trade because the lower credit score could impact the rate you pay on a home mortgage, and auto loan/lease, even the insurance companies that will work with you.

When it comes to the question of “how to close a credit card,” a generally better strategy is to not cancel the card and to, instead, stuff the card into a lockbox or maybe a bank safe-deposit box and leave it there, unused. The credit line stays open, your available credit doesn’t decrease, and you have no payments to worry about. And there’s no impact to your credit score.

The one caveat is if the card imposes an annual fee. You don’t want that unnecessary cost. So, call the card issuer and announce you’re going to close the card unless they can eliminate the fee. Some will work with you. Some won’t. If they won’t, you have to decide if the annual cost is worth having that credit line open.

Does Closing A Card Hurt Your Credit Score?

In the short term, closing a credit card account might negatively impact your credit score, but that will only be temporary.

Credit scores rely on a bunch of black-box math that the credit agencies don’t completely divulge. But among the various factors are length of credit history and credit utilization. If you close an account that’s relatively new (at least in terms of your oldest credit card) then your credit score should not be affected.

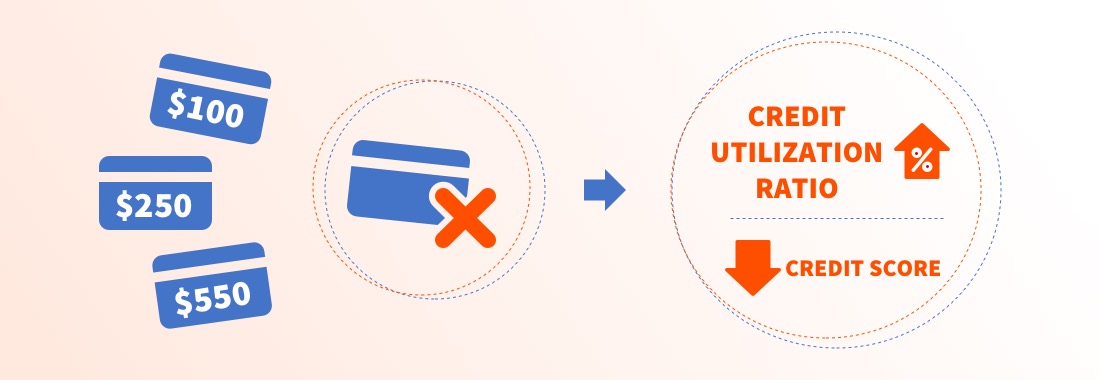

But when you cancel a credit card you are, by definition, decreasing your overall credit limit, and that can impact your credit score because increases your credit utilization.

Let’s say you have two credit cards with a combined credit limit of $25,000. Card #1 has a $15,000 limit and Card #2 has a $10,000 limit. You owe no money on Card #1, but you owe $5,000 on Card $2.

Your credit utilization is 20% (5,000 / 25,000).

Now let’s say you close Card #1 because you’re not using it and there’s no balance on it.

Suddenly your credit utilization soars to 50% (5,000 / 10,000).

What If I Just Want To Switch To A Better Credit Card?

Credit card companies offer a lot of bad credit cards, no doubt. And if you have one, then it makes a lot of sense to replace it with a card that has

Even then, though, it’s generally wiser to keep that credit card open and roll any existing balance onto the new card. Then, just put that old card away for safekeeping, but leave that credit card account open. (Again, the caveat is the annual fee).

A few cards to consider as replacements:

Capital One Quicksilver Cash Rewards: No annual fee. Valuable sign-up bonus after spending minimum required amount. You earn nice

VentureOne From Capital One: No annual fee. Great 20,000-mile

What If I Still Want To Cancel A Credit Card?

Nothing is stopping you from closing your credit card account. But the process of how to cancel a credit card involves more than cutting your old card to pieces and tossing them into the trash.

Here are the steps you need to follow to properly close a card:

1. Pay off the balance in full, or open a new credit card (with a

2. Cancel automatic charges linked to your old card (transfer them to the new card or another existing card, if necessary). Forget this step, and the company charging your card every month will be told your account is closed the next time it tries to charge your card, and chances are your service with that provider will be interrupted or cancelled. To simplify this process, log into your credit-card account and go through the last six or months of statements to find the automatic charges (some might be quarterly or semi-annually, so that’s why you want to go back more than half a year).

3. Redeem any rewards still in your account. When you close a credit card account, you typically forfeit whatever

4. Call your credit card company tell customer service you want to close your credit card account. You will undoubtedly be transferred to the customer retention department and offered special perks aimed at keeping you as a customer – bonus miles, a special interest rate or other enticements. If those appeal to you, grab them. You win. If you still want to cancel your credit card, politely decline and the customer-service agent will process the closure.

Pro tip: Always request a letter in writing from your credit card company, noting that the account was “closed by consumer” with a $0 balance. This is to protect yourself, because credit bureaus do screw up, and that letter can help you resolve any kind of discrepancy that might show up in your credit file.

5. Watch your mailbox. Look for the confirmation letter you requested, and file it, just in case you need it later. This is more important than it sounds. An credit card account closed in good standing can have a positive impact on your credit report for as many as 10 years. So, you want documentary proof in the event you have to contest a negative notation in your credit file with a credit bureau.

6. Check your credit report. Your old credit card company will take up to 60 days to report the account closure to the various credit bureaus. So, watch your credit report over the next two months to be sure that the account was closed properly. By that, I mean you want to be sure your file says this account was “closed by consumer” (or similar language). If it says “closed by creditor,” that has negative connotations and can hurt your credit score … thus, the reason you want that letter from your credit-card issuer confirming that you requested the account’s closure.

The Wrap Up

Credit cards are a fact of life, and they are going to be even more so as societies move increasingly toward a cashless world. As a savvy financial consumer, you need to know not just how to find the

Moreover, just because credit cards are necessary, doesn’t mean you should be stuck with a bad one. Learn how to properly close a bad credit card so that you can replace it with

And we want to know: What’s the best offer you’ve been given when trying to close a credit card?

Did a card issuer bombard you with bonus miles or other rewards?

Let us know in the comments below.