Your trip is booked, your bags are packed, and you’re ready to go. Chances are the last thing on your mind is how you’re going to save money on currency conversion fees, securing pocket cash and on your foreign purchases.

These expenses can add up though and without some upfront planning, you’ll return from your holiday with a bank or credit card statement full of fees. Minimal time invested before you go can result in reducing transaction fees, avoiding overcharges for foreign travel expenses and even earning rewards while you’re traveling.

Use a Credit Card That has no Foreign Transaction Fees

Foreign transaction fees charged by your credit card issuer apply to every foreign purchase you make when you travel. One of the best ways to save money when spending abroad is to utilize a credit card that doesn’t charge such a fee. If a credit card doesn’t explicitly state that there is no foreign transaction fee, it probably charges one.

Since the average foreign transaction fee can range from 1 to 3% of the purchase amount you can immediately save at least that much by using a credit card that doesn’t charge a fee. Examples of cards that do not have foreign transaction fees are Discover It and Discover It Miles, Chase Sapphire Preferred, Barclay Arrival Plus, and the VentureOne Rewards Card.

Beware and Refuse Dynamic Currency Conversion

It may seem convenient and simple to pay your foreign hotel bill in U.S. dollars. Paying in U.S. dollars lets you know exactly how much you’ll be charged and you won’t have to deal with figuring out currency exchanges. The problem with this scenario is that the U.S. dollar option may cost far more than paying in local currency. The entire process is known as dynamic currency conversion (DCC) and it can hurt you.

When you pay in U.S. dollars instead of the local foreign currency, the U.S. dollar then needs to be converted to the local currency in order to pay the merchant. The exchange rate charged is not favorable and there are service fees that are added. These fees go to the provider facilitating the currency transaction.

For example, your final hotel bill in Paris totals 400 Euro. You’re not really sure how much that is in U.S. dollars but there is the option to pay $490. You might assume this amount was calculated using the current foreign exchange rate and you figure it’s about the right amount for the room you booked so you select to pay that total in U.S. dollars.

At this point, the transaction is then processed at the provider’s unfavorable exchange rate, fees are added and the final total reflecting the higher amount will ultimately show on your credit card statement. If you had selected to pay in the local currency, your bank would have converted the 400 Euro using the current exchange rate and in this case charged the $470 to your credit card.

You may encounter Dynamic Currency Conversion at hotels, restaurants, retail merchants, and transportation providers. Since it’s difficult to dispute a transaction once you’ve signed for it, you’ll want to avoid the situation at the point of sale. Review any receipts you sign and select the local currency for payment. Do not sign a bill that is totaled in U.S. dollars and request that it be voided. Additionally, make sure that the box next to the total in U.S. dollars is not already checked for you.

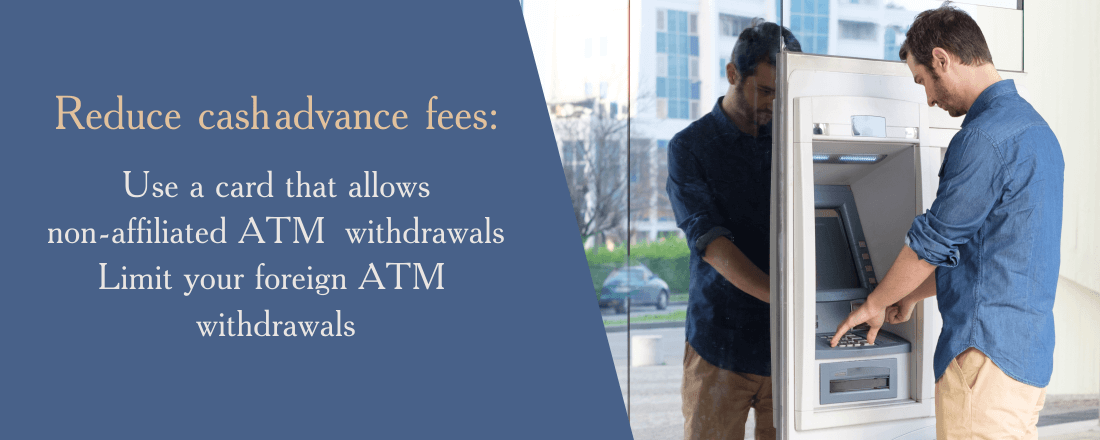

Minimize Foreign ATM Fees

There are several charges that come into play when using your debit card to secure local currency from an ATM abroad. You’ll first be charged a foreign transaction fee to withdraw funds from your U.S. based account and convert those dollars to the local currency in the country you’re withdrawing funds. The second charge could be a fee charged by your bank for using an ATM that is not in your bank’s network. The third could be a fee charged by the foreign ATM you’re using. Despite the fees, using an ATM to obtain local currency is still a very viable option for securing cash during your trip.

To minimize foreign ATM fees, find a debit card that allows at least a few non-affiliated ATM withdrawals per month. During your trip limit your foreign ATM withdrawals to one, if possible, to avoid multiple fees. You could also open an account with an institution such as Discover Bank, Charles Schwab, or First Republic Bank which waive or refund ATM and conversion fees.

Local credit unions can also be a good option for securing a debit card that minimizes foreign ATM fees. Different terms and conditions apply for each account and the network of affiliated ATMs varies significantly. Opening a new account just for travel may seem excessive but it’s a worthy cost-saving step if you travel often.

Use a Rewards-Earning Credit Card

Many credit cards earn extra points, cash back or miles on travel, dining, gas or other bonus categories. Some credit cards even earn multiple points for every dollar spent on the card. Using your rewards-earning credit card for your foreign purchases will not only result in getting charged the best currency conversion rate when you make the purchase, you’ll also be earning rewards on those purchases.

Anticipate the expenses you’ll be incurring during your travels, select the credit cards that earn rewards on those specific categories and spend accordingly, prioritizing those credit cards that have no foreign transaction fees.

The Bottom Line

You won’t go broke by failing to execute any of this information during a short holiday excursion. If you travel often or if you’re spending thousands of dollars on an epic vacation, however, you could be wasting a lot of money on fees and potential overcharges. A little advanced planning could help you avoid those expenses and put travel dollars back in your pocket.