So, Apple is getting into the credit card business with what it calls a truly game-changing take on the credit card. But is Apple’s claim that the card has no hidden fees accurate?

Well, no!

In fact, Apple might well have announced the most-expensive hidden fee in the history of credit cards!

This Article Will Cover

- First, Let’s Go Over What Apple’s New Card Offers

- No iPhone – No Card For You

- It Gets Worse

- If You Want A True No-fee Credit Card, Then Consider One Of These

- If You Want A Metal Credit Card

First, Let’s Go Over What Apple’s New Card Offers

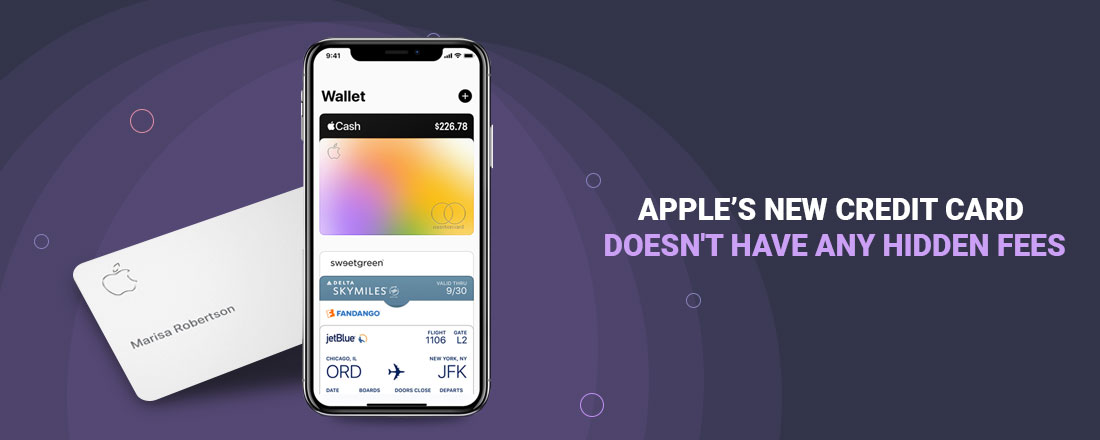

Apple launches its new card this summer, in partnership with Mastercard and Goldman Sachs, the bank will issue the card. The card exists virtually on your iPhone, though you can request a physical, titanium metal card if you wish. And given the status of metal cards – and the idea of flaunting a sleek Apple card – I’m betting the vast majority of cardholders will request the physical card.

Apple says the card will charge

As well, the Apple card offer will rely on two-factor authentication for Apple Pay, which currently allows users to store their other credit cards in the digital wallet on their iPhone. To make a purchase, an Apple cardholder will need to log into their phone and approve the purchase with a face ID or a fingerprint.

And that right there tells you that the Apple card has what I’ll bet is the largest hidden fees in the credit card world. You have to own an iPhone to use the card!

No iPhone – No Card For You

So just to join the party you have to go buy an iPhone if you don’t have one.

And not just any iPhone, you need an iPhone with face ID or fingerprint technology. Sure, the iPhone 5s and 6 have fingerprint technology, but early betting is that you will need at least an iPhone 8 to use an Apple card — maybe an iPhone 7 at the oldest.

I know many people still using an iPhone 5 or 6. For them to use the new Apple card, they’d likely have to upgrade to a more expensive phone.

That is a fee, pure and simple!

It Gets Worse

At the end of the day, a credit card is primarily to buy things without the need for a wad of cash or the time-consuming need to write a check. To that end, you have

Apple reportedly is already looking to dump the iPhone 7 later this year in terms of support. So that means at some point, an iPhone 7 user with an Apple card will be forced to upgrade to a new phone. And with new iPhone models having now cracked the $1,000 threshold … well it’s pretty obvious Apple might not be charging an annual fee directly to have an Apple card, but the consumer is going to pay a very real cost.

A $1,000 iPhone X is more than a decade’s worth of $95 annual fees! Or roughly two years of annual fees for the American Express Platinum card or ten years of annual fee for the credit card Capital One Venture Rewards. Both of them are valuable metal credit cards with lucrative bonuses.

If You Want A True No-fee Credit Card, Then Consider One Of These

Capital One VentureOne Rewards: Enjoy a one-time bonus of 20,000 miles once you spend $1,000 on purchases within 3 months from account opening, equal to $200 in travel.

1.25X miles on every purchase, every day and pay no annual fee.

$0 annual fee and no foreign transaction fees

No foreign transaction fees.

Bank of America Cash Rewards: Online $150 cash rewards bonus after making at least $500 in purchases in the first 90 days of your account opening. 3% cash back in the category of your choice: gas, online shopping, dining, travel, drug stores, or home improvement/furnishings. 2% cash back at grocery stores and wholesale clubs. 1% cash back on all other purchases

. No annual fee.

Chase Freedom: 0% rate for 15 months on purchases and balance transfers. $150 cash bonus after spending $500 in first 3 months. 5% cash back on up to $1,500 in combined purchases in bonus categories each quarter. Unlimited 1% cash back on all other purchases. No annual fee.

If You Want A Metal Credit Card

Capital One Venture Rewards: 50,000 bonus miles after spending $3,000 in first 3 months. 2x miles on every purchase. Annual fee: $0 intro for first year; $95 after that thereafter.

Capital One Savor Cash Rewards: $300 cash back bonus after spending $3,000 in the first 3 months. Unlimited 4% cash back on dining and entertainment expenses; 2% cash back at grocery stores; 1% back on all other purchases. In addition, because of a new partnership with Vivid Seats, get 8% cash back on tickets for live shows, concerts, sporting events, and other similar events through May 2020. Annual fee: $0 intro for first year; $95 after that thereafter.

The Wrap Up

Apple certainly changed the game when it first unleashed the original iPhone. Since then, the company has been looking to bottle lightning for a second time. Alas, the Apple credit card is that lightning strike.

Apple might play up the idea of no fees, but the operational reality is that you have to own an iPhone to have an Apple card, and you will undoubtedly need to upgrade your phone on time. Given the cost of an iPhone now, the cost of that purchase is a substantial hidden fee consumers will pay to get or keep their Apple credit card.

So think carefully before rushing to apply for your own Apple card. And ask yourself if it’s really worth the fee you will pay … or are you better off choosing a card that truly offers no hidden fees and comes with

But we want to know: What do you think of Apple’s new credit card – will you get one, despite having to upgrade your phone at some point to keep your card?

Let us know in the comment section below.