American Express sometimes offers 100,000-point

Though it was only available for less than a day, word spread quickly and many travel enthusiasts were able to sign up before the link was taken down. In the months that ensued, many people reported that Amex had frozen their accounts and clawed back the points from the

We’ll tell you how to avoid this and other problems, as well as covering the ins and outs of American Expresses sign-up bonus policies.

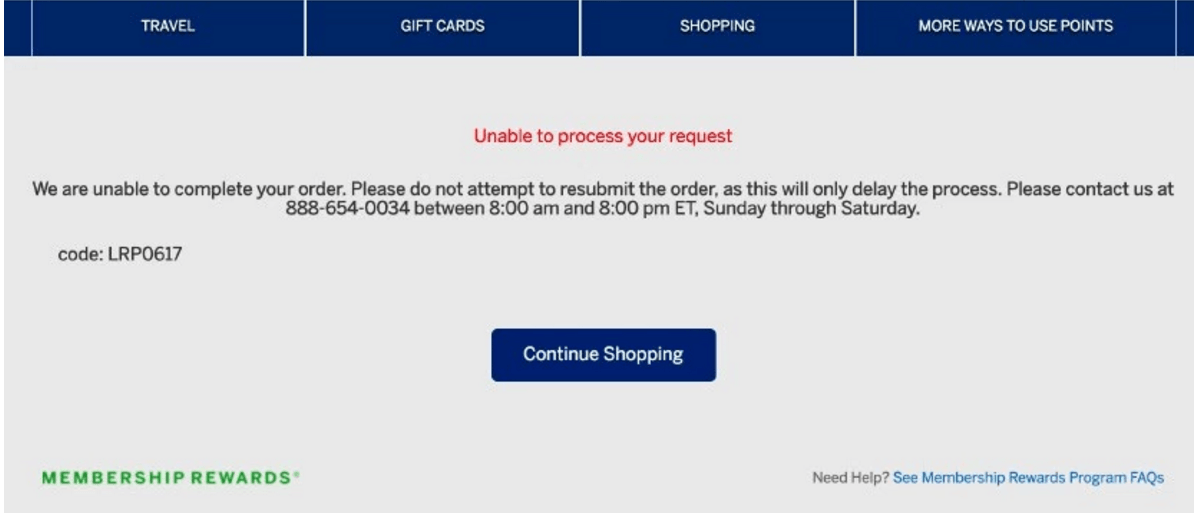

When this incident happened, cardholders would often first encounter an error message when attempting to transfer points out of their account, such as the one below:

As people shared their data points and attempted to find a common thread, it became apparent that Amex was clawing back bonuses for violating the terms and conditions of meeting the minimum spend.

Some people who reported problems engaged in ill-advised behavior, such as making large purchases to exceed the minimum spending requirement, then returning the items after the points have posted. While this sort of thing is clearly not permitted by Amex and other issuers, other people reported having bonuses taken away from them for other questionable behavior, such as manufactured spending techniques.

Amex’s terms and conditions clearly state that certain transactions will not count toward minimum spend including “purchases or reloading of prepaid cards; or purchases of other cash equivalents.” Manufactured spending is a no-no, and Amex will crack down on this behavior.

There are enough manufactured spending-related reports of accounts being frozen and points being revoked that you should “play it safe” when it comes to meeting minimum spending requirements.

This topic is relevant now because there are occasionally publicly available links for 100,000-point sign-up bonuses on the personal Platinum card and there is currently a public offer of 100,000 points on the Business Platinum card.

The minimum spending requirement is quite hefty on the Business Platinum card. It is a two-tiered bonus—50,000 points for $10,000 in spend and 50,000 more points for an additional $15,000 in spend within the first 3 months of card membership.

Between the personal and

Meeting High Minimum Spending Requirements Without Manufactured Spending

Here are a variety of ways to meet minimum spending requirements without using any prepaid cards or other things that may be considered a violation of terms by Amex.

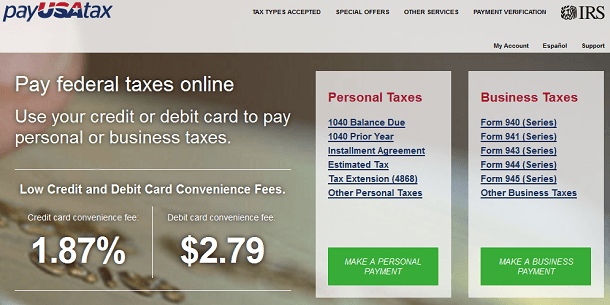

1. Pay Federal Taxes With a Credit Card

This might not be so useful until next tax season, but if you have a large tax bill, paying it could be an easy way to meet a minimum spending requirement. Thankfully, the Federal government accepts tax payments via credit card.

Remember you can pay “estimated” taxes in advance and get a refund for the difference if your actual tax liability ends up being lower than the amount paid. Fees range from 1.87% to 2.25%, depending on the payment processor.

2. Invest in Kiva Loans

Kiva is an organization that makes micro-loans to be people in third world countries to help fund

However, this method does come with other potential costs. Kiva loans have an average default rate of slightly less than 1% which can be considered the cost of this form of spending. To reduce your risk, invest in a diversified portfolio of small loans rather than a small number of large loans.

Also, loans take several months to be paid back, so this method will require you to float funds (the payment structure varies from loan to loan, so read carefully before investing).

3. Fund Daily Fantasy Sports Accounts

If you’re into fantasy sports, using websites such as Fanduel.com can be a good way to meet a minimum spend. The site allows you to fund your account with a

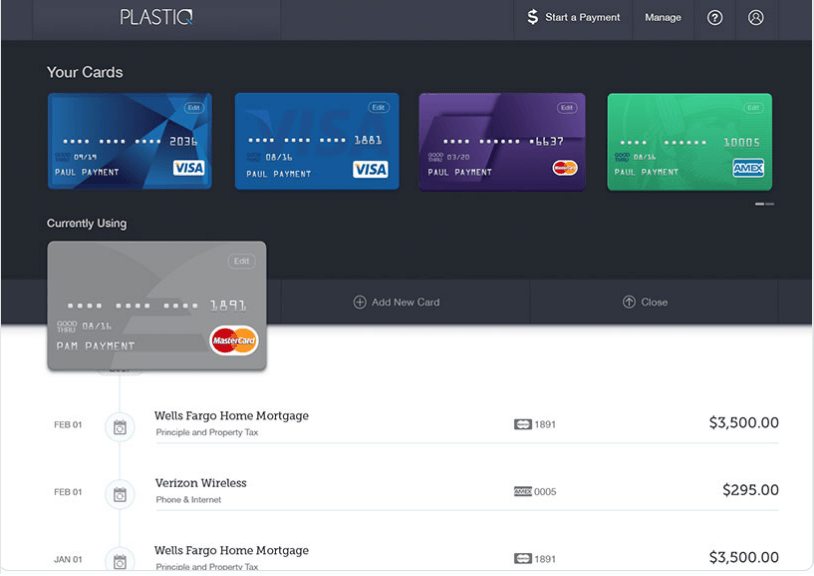

4. Pay Bills Using Plastiq

Plastiq.com is a website that allows you to pay bills that you couldn’t normally pay directly with a credit card, such as mortgages or other loans. Plastiq charges your credit card and then sends the payment, either by ACH or physical check, to the account you specify. If they payee is in their database it will be sent via ACH, otherwise they will mail a physical check.

Plastiq charges a 2.5% fee for all credit card payments. Make sure the points you earn outweigh the fees you incur. Also, note that if Plastiq sends a physical check to your payee, it will likely take at least a week for the funds to arrive. We recommend giving yourself a buffer of at least 2 weeks to ensure the payment arrives on time and no late fees are incurred.