You have probably heard of a balance transfer, but how does it work and will it really save you money?

Transferring a balance can provide some relief from that debt keeping you awake at night because you can save interest payments if you transfer your balance to a card with a 0% APR. You will also be able to pay off your debt faster since you will only be paying the actual money owed, rather than the interest charges it’s been accruing.

A balance transfer is when you take an existing credit card balance from one card and move it to another, generally one with a lower interest rate or a zero percent interest introductory offer.

If you have credit card debt and are paying high interest, this post may help you save money and be free of debt soon.

Why you might need a balance transfer

Sometimes you get caught in a cycle where you are trying to get out of debt, but if you are just making the minimum payment due you are probably only paying enough to the meet the interest payments. But what can you do?

The answer is: transfer from your high-interest card to a new card with a zero percent introductory period, so you can save money on interest and pay your balance faster.

Keep in mind that you may pay a transfer fee to move the debt from one card to another, but the benefits of not paying interest usually outweigh the cost of making the transfer.

Time to act: How does a balance transfer work?

There are different ways to get a balance transfer. You can accept an offer from a new card issuer, or you can check on an offer from one of your current credit cards. What you can’t do is to transfer debt between accounts from the same bank.

To complete the transfer you will need:

- The account number of the card or cards you want to pay off

- The total balance to be transferred

Balances can be paid in full or part with a balance transfer, depending on what you owe and how much of a credit line you receive for the balance transfer.

Once approved for the transfer, your credit card issuer will contact your former bank and pay off your card balance. It could take weeks, so it’s very important for you to continue to make payments on the account until the transfer is complete.

Is my credit score at risk when I transfer a balance?

The quick answer is no, it likely won’t affect your score if you follow the rules outlined below. It might even help it. Factors like credit utilization, on-time payments, and credit history are important and can even make your score higher.

Rule #1 Always make your payments on time

Your history of on-time payments indicates how responsible you are with your financial obligations. To lenders, your payment history tells them what you are likely going to do in the future if they lend you money. Even if you only make your minimum monthly payment, you need to make all payments on-time.

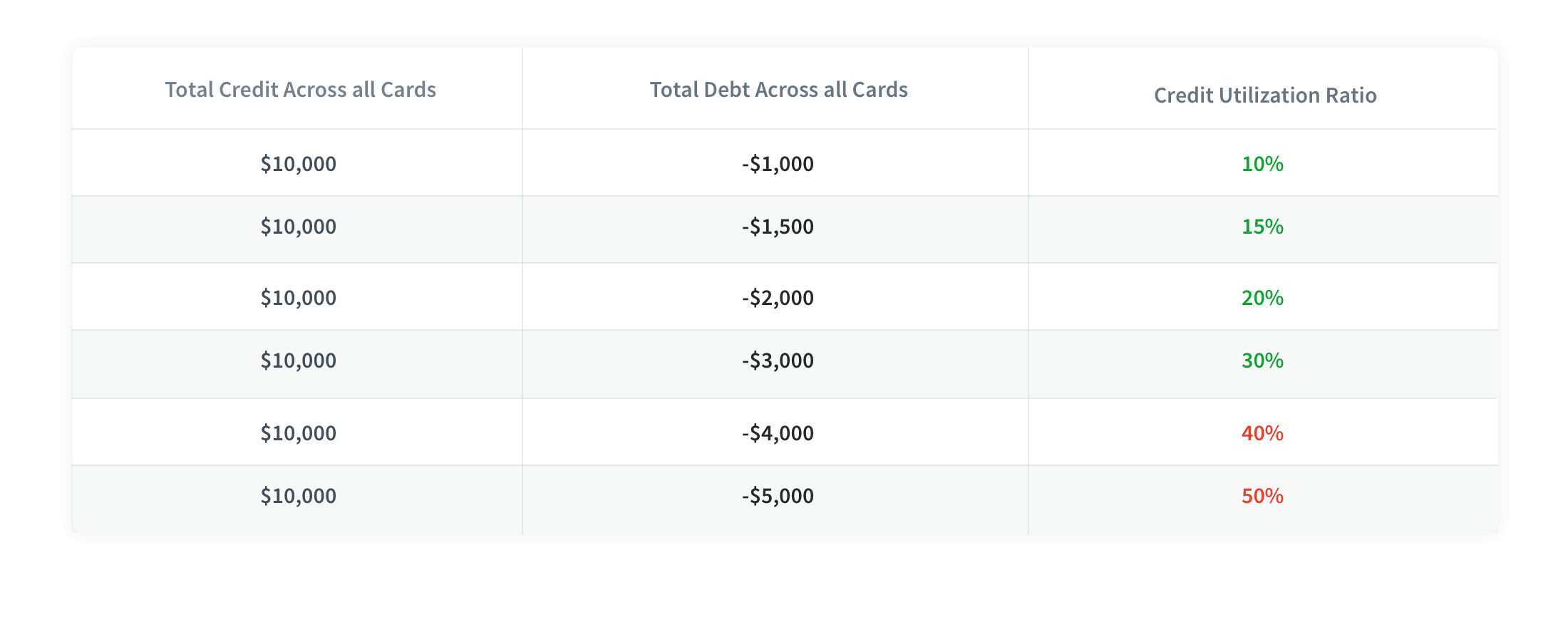

Rule #2 Keep your credit utilization below 30%

Credit companies look for signs that you will be responsible if they lend you money, so the less you use your credit the better your score. Now that doesn’t mean you can’t channel your everyday spending through your card. Utilization refers to the total amount you owe vs. your total credit line. Using less than 30% of your available credit is a good sign.

Here is a chart to help you understand the credit utilization ratio:

The utilization rate is calculated based on all credit cards you have, not just one. If you have three credit cards with a $1,000 limit each card and the outstanding balance on one of these cards is $300, your rate is 10% ($3,000/$300.) If your credit utilization is over 30%, you would need to get a credit card with a higher credit limit that the balance you are going to transfer in order to keep the utilization low.

Rule #3 Never apply for more than one credit card at a time

Every time you apply for a credit card, the card issuer sends a hard inquiry to a credit bureau. If lenders see too many inquiries at once that can be viewed as a sign that you are desperate for credit. Also, opening too many new accounts in a short period of time could point to credit problems. Banks see these two behaviors as risky.

If you get approved from the card issuer, it means that they trust you and your credit score may even increase. However, if your inquiry is rejected, your score can be lowered.

Rule #4 Don’t close your old card

It’s also important to keep in mind that credit history matters and the age of your oldest accounts indicates your experience handling credit. A good tip is to keep your oldest accounts open and in good standing so all that good credit history doesn’t drop off your credit report.

Understanding and Choosing the Right Option

A balance transfer may seem like a really good option, but it only makes sense if you save money and you can improve your credit score as a result.

Before making a decision on whether to make a balance transfer you should compare factors like how much money you want to transfer, how low the new interest rate is, and how much the transfer fees will be.

Who Are You Paying More?

The best starting point is to identify which credit cards make you pay the highest interest and which ones have the biggest balances. Those cards would be the ones you want to cut down first as they are the most expensive to carry a balance on.

You can transfer one or more cards using this method. By consolidating several accounts into one you will have less monthly payments and it will also be easier to manage.

What is a balance transfer fee and how to avoid it?

Banks have fees. That’s the norm. For a credit card balance transfer, you will usually pay between 3% and 5% of the amount that will be transferred. If you transfer $10,000 and the fee is 3% for example, you will end up with a $10,300 debt as the fee of $300 would be added to the balance.

However, if you have a good to excellent credit score, you can probably avoid the balance transfer fee by using the credit cards below.

Best Balance Transfer Credit Cards with Zero Fees

If your score is good enough you can likely get one of these zero fee cards:

Best Balance Transfer Credit Cards with 3% Fees

A good or better credit score can makes the difference and save you even more money with a balance transfer.

Watch Out: 4 Things You Need to Know When Transfer is Complete

It’s not only about saving money on interest. It is also about becoming more responsible overall when it comes to accruing debt.

1. Never use this card for new purchases

One of the biggest traps for customers that transfer their balance to a zero percent or low-interest card is to believe that new purchases with the new credit card also get a pass on interest. This is not always the case, so be sure to read the fine print on your agreement. New purchases are usually subject to the card’s regular interest rate. Some include a zero percent interest introductory period on purchases, but not all.

Another mistake is to take out a cash advance. This is always a big no-no. Cash advances carry a higher interest rate than the card does for purchases and there is no grace period so the interest kicks in right away. Read the terms and conditions to get all the details.

2. Don’t miss the promo expiration date!

It’s important to keep an eye on the date your zero or low interest rate expires. Sometimes it’s a year and can be as much as 18 months or more, but once that time has passed the interest will start again, so it’s important to try and pay off as much of your debt before that date so you don’t end up back in the vicious cycle of paying high interest.

If you can manage to make enough payments to reduce your debt to nothing, then you will start with a clean slate. Be sure to spend carefully and pay off your balance every month to avoid getting into debt again.

3. Don’t miss a payment. Never. Period!

If you don’t make the minimum payments your promotional rate may be canceled and you will be charged the regular interest rate or possibly even a higher one. That would defeat the purpose of the balance transfer.

4. Stay on budget

If you are thinking about a balance transfer it is because you are trying to improve your finances. So make sure you have a plan to pay down your debt. If you don’t have a plan, you should make one.

After deciding which card to apply for, you should figure out how much money you can pay every month. You can always pay more to unload debt sooner, but you should have a minimum amount in mind that will help you reduce or eliminate your debt load.

Is it a good idea to do a balance transfer?

Yes, it is a great idea for many people, especially if you spent more than you should have during the holidays. A balance transfer is a great tool to save money and pay debt faster. If managed correctly, it will also improve your credit score, so it will be a win-win situation.