Whenever you get a new credit card, you might be a little baffled by the long string of numbers. Yes, there are a lot of people with credit cards, and the issuers need to have a variety of numbers in order to make sure every person gets a unique identifying number. But that’s not the only reason. Every one of those numbers on the front of your card (and the three or four on the back) serve a purpose.

Many of the digits are there to help identify you as the owner of the credit account. Others are to help protect you from fraudulent purchases. Each of those numbers are there to create an account that allows you to buy what you need, and pay for it later. Take a look at the five most important aspects of your credit card number. We’ll help you understand why you should care about them, and how they help to protect you.

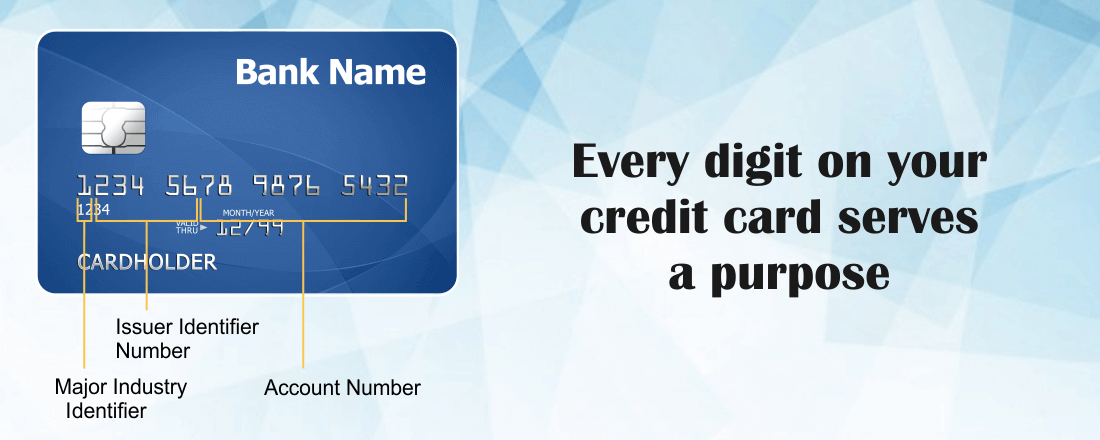

The First Digit: the Major Industry Identifier

Every industry that issues a credit card has a number that goes along with it. This number is the first digit on any card issued, a requisite standardized by the international organization for standardization back in 1989. There are a variety of different digits, but the ones that appear most often are three, four and five. Why these numbers? Because you’re most likely to have a card that starts with one of them.

Three, or more commonly 34 or 37, is used by American Express. The number 3 represents the travel/entertainment category, and all Amex cards are issued starting with this number.

Four is

Five is

The other numbers are less used and include:

- 1 & 2 – Cards issued by airlines

- 6 – Merchandising cards

- 7 – Petroleum

- 8 – Telecommunications

- 9 – National Assignment

Why this is useful: Most of us know whether we have a Visa, Mastercard, or one of the other small payment networks. But these numbers aren’t really meant for you as much as they are meant for the system. The first number quickly routes any purchases to the appropriate creditor.

The Next 5: the Issuer Identifier Number

The first six digits, the Major Industry Identifier and the following five digits, determine the Issuer Identifier Number (or the Bank Identifier Number). For smaller institutions these will always be the same, for larger institutions they have a variety of six digit numbers. If you have two accounts at the same bank, let’s say a credit card and a debit card, check the numbers on the front. The first six numbers (sometimes even more than the first six) are exactly the same.

Why this is useful: Just like the first digit in your credit card number, these are for routing charges quickly to the right place. Think of it like your address. The first digit gets it to the right area (kind of like your city and state); the Issuer Identifier Number gets it to the right part of the city (kind of like your zip code). Next is your actual address.

The Account Number

All of the numbers that follow the first six are unique to your account. These six to 11 digits are what identify you as the account holder and the owner of the card. There may be some overlap if you have two accounts at the same bank, but your account is the only one with these numbers.

Why this is useful: When you make a charge, the process goes through a series of checks so that it ends up at the correct account holder. Your unique account number is what will ensure that only your charges end up on your account.

The Safety Number

Today, with the security numbers and the chip, it’s harder than ever to forge a credit card. But that doesn’t stop people from trying, and often succeeding. One method to prevent credit card fraud is the final digit on your card. Using a complex algorithm, all of the other digits on the card can determine exactly what the final number is going to be. So if someone happens to steal the majority of your card information, but they don’t know the exact account number, they will have trouble creating a fake account number without knowing that algorithm.

Why this is useful: Credit cards are easily forged, you can often do so with nothing but a magnetic key card to a hotel and some fancy software. But unless you have stolen the numbers from someone else and it’s exact, that safety number prevents the card from working.

The Numbers on the Back

The safety digit, however, isn’t always enough; especially in the modern era of shopping online. In the past a criminal could have simply memorized your card number and been able to duplicate your card. Now, there’s more to it. These security numbers are called a CCV (Card Code Verification) or a CVV (Card Verification Value), and they’re generally three digits long (in the case of American Express, they are four digits long). In reality, they are security measures put into play by the card companies themselves, and there is no set standard that cards must adhere to.

Why this is useful: Any added protection is a good thing. While it may be cumbersome to type in the additional information, these simple numbers have probably saved you from suffering from identity theft.

Understanding Your Credit Card Number

If you’re like most people, you probably thought your credit card was a random string of computer generated numbers. Who knew there was so much more to them!

Understanding how money (and in this case, credit) works will set you far above your peers when it comes to financial literacy. Knowing the meaning behind the card numbers helps you to understand all of the safety measures put into place to ensure that your identity isn’t stolen, and you now have better knowledge about why you have those extra digits.