How much will you spend on holiday shopping this year? According to

When you add to that the amount spent on food, entertainment

Shop Responsibly

The most important tip of all is not to overdo it. Travel hackers know they should not charge more than they can pay off by the end of the month.

Carrying a balance on a rewards card increases your cost of using that card. Interest rates alone, even on a modest balance, can easily eat up any savings or bonuses you earn. Stay disciplined.

Remember these words of wisdom: You didn’t save $250 on a $1,000 purchase–You paid $750! Don’t get lulled into irresponsible spending just because it’s the holidays and everything seems to be on sale.

The 0% Exception

The lone exception to not carrying a balance could be a 0% introductory interest rate card. This could provide an easy way to manage a large purchase. Pay it off in less than 12 months or whatever the introductory period is, and still pay no interest.

A good

It’s important with 0% cards to keep your minimum monthly payment high enough to ensure you pay off the card before the introductory period expires. Don’t get caught near the end of the period trying to find enough money to pay the rest of the balance.

Use It, Don’t Lose It

Reward cards typically offer miles, points or cash back. Make sure your card is one that earns rewards you will actually use.

Bonus miles on an infrequently used or unavailable airline will expire. As will free nights at a hotel chain you hate or one located in areas where you never travel.

Think Sign-up Bonus

It isn’t always easy to take advantage of some of the better sign-up bonuses because the minimum spend level is high for some people. Fortunately, holiday shopping, if planned well, is tailor-made to help meet the spending requirement.

If you’ve been thinking of signing up for one of those 50,000 or even 100,000 signup bonus cards with a $3,000 or $4,000 spend requirement over three months, now may be the time to pull the trigger.

The Chase Sapphire Reserve card offers 100,000 bonus points after you spend $4,000 in the first 3 months. It offers 3X points on travel and dining and offers several additional perks.

Target Travel

Many travel credit cards issue higher rewards or reward rates for travel-related buys. Some do so only for flights or hotels booked through their websites while others are more flexible.

Also, make sure any money you spend on travel also earns you a reward. Not to mention travel credit cards often offer additional perks such as travel insurance, delayed or lost baggage coverage and free checked bags. Access to an airport lounge can be a lifesaver during the often-hectic holiday travel season.

For example, the Chase Sapphire Preferred card offers a 50,000 point sign-up bonus after spending $4,000 in the first 3 months with 2X points on travel and dining and many of the other perks mentioned above.

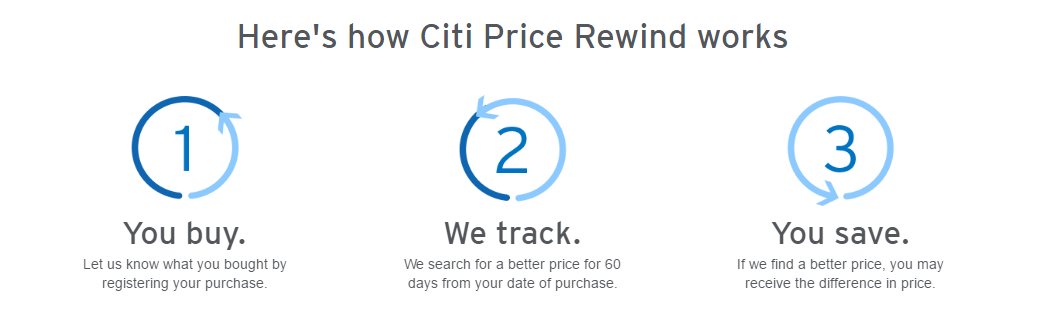

Price Protection and More

Speaking of additional perks, many cards offer additional protections that go unused because consumers don’t know they exist. Common perks include purchase protection and extended warranties—perfect perks for the holiday season!

Less common perks

Think Outside the Rewards Box

Sometimes it matters where you buy your gifts. Some credit cards offer higher rewards at department stores. Others boost rewards for shopping at Amazon.com or other online retailers. Some offers change quarterly. Check the website for your rewards cards to see if you get bonuses for shopping at certain retailers.

Buying gifts and travel are only part of holiday spending. Hosting a holiday meal or party could be another large holiday expense. If you plan to spend a considerable amount on groceries, it might be worth seeking a card that pays a higher reward rate on food purchases.

Along the same lines, if your company allows you to use your personal credit card for company purchases and reimburses you, offer to buy everything needed for the company party.

Spend Your Points Wisely

All of those points will add up fast but figuring out the best way to use them in exchange for travel isn’t always easy. Check out our homepage at rewardexpert.com. Simply enter your travel information and our interactive wizard will tell you

Finally

Don’t just head to the stores and throw down your credit card without thinking about how your credit card could work for you. Take advantage of the rewards and perks that come with the card. And if your card is stingy with the rewards it offers, it might be time for a new card.