Millions of small businesses call Canada home. In fact, according to the most recent data from Innovation, Science and Economic Development Canada (ISED), a department of the Canadian government formerly known as Industry Canada, nearly 98 percent of the country’s total employer businesses are classified as “small,” with fewer than 100 paid employees.

It’s a demographic that Thinking Capital, an early leader in the fintech industry, knows well. The alternative finance company’s co-founder and CEO, Jeff Mitelman, spoke to RewardExpert about Thinking Capital’s origins as well as its mission to simplify borrowing for Canadian small businesses.

Customers in More than 300 Industries

“Our history is in the payments business,” Mitelman explained. “We had quite a large base of small business customers, and in speaking to them, we learned that one of their pain points was accessing financing. We built out a financing product as a value-added proposition for our payments customers, and that’s really the early genesis of Thinking Capital.”

Since its founding in 2006 as CFC, a subsidiary of CARDEX, and subsequent rebranding as Thinking Capital in 2015, the Canadian leader in alternative financing for small business has helped more than 14,000 organizations reach their full potential.

“By the end of 2018, we will have funded $1 billion into Canadian small businesses,” Mitelman added.

Thinking Capital’s customers include small business owners in more than 300 industries in need of capital for renovations, inventory and equipment purchases, marketing and other business expenses. To qualify for a small business loan through Thinking Capital, customers must have a business history of at least six months and average monthly sales of at least $7,000.

“Our customers are very much from Main Street,” Mitelman said. “They are your local dry cleaners and your favorite pizza shops. They are the corner stores you go to for quick groceries. They are owner-operated businesses that have been around for generations and e-commerce businesses that have figured out how to sell unique products around the world.”

Supporting the Way Small Businesses Need to Borrow

While there are other small business lenders offering fixed payment and flexible payment loans, Mitelman explained that Thinking Capital operates differently.

“We’re quite focused on supporting the way the small business customer seeks to borrow,” he said. “A good example would be that most of our enquiries come through in the middle of the night. Obviously, you can’t go into a traditional bank branch at that time. So, rather than thinking about our products as simply fixed payment or flexible payment, we tweak them in ways that support the ebbs and flows of small business cash flow and allow borrowers to access additional funding while still in repayment.”

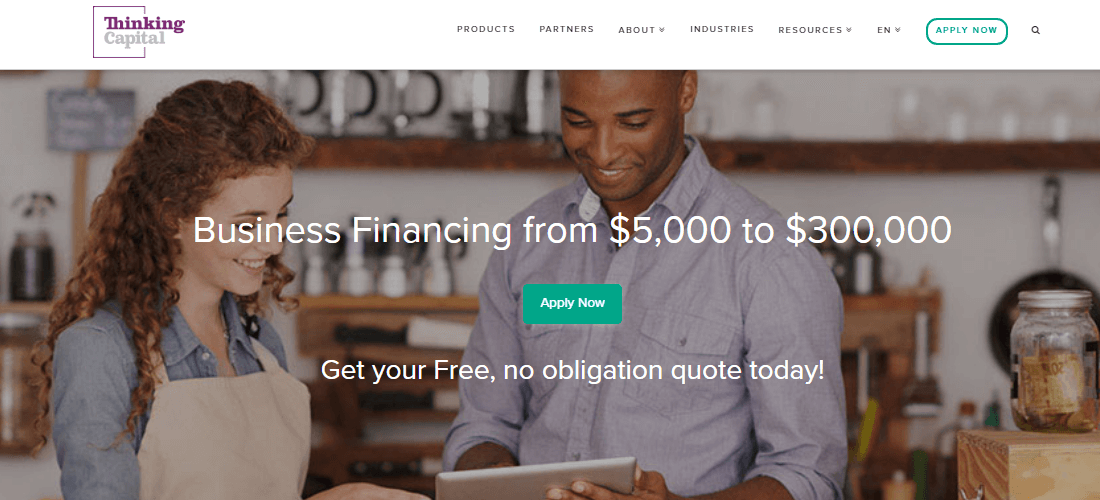

Small business owners can borrow as little as $5,000 to as much as $300,000 and generally receive a lending decision and funds in as little as 24 hours.

“Our lending decisions are made algorithmically,” Mitelman explained. “Essentially, what that means is that we collect data from a number of sources, such as bank accounts, payment providers and accounting platforms, and then use a benchmarking system that allows us to very quickly qualify the creditworthiness of a prospective borrower in a way that is materially different from the data you would get from a credit bureau.”

Mitelman said this quick turnaround is vital because small businesses often have unforeseen expenses and opportunities. “We’re quite good at responding to that,” he added. “If they have an opportunity to buy widgets, and they can buy them at a significant discount but need to act quickly, we check that box.”

Thinking Capital does not require collateral or perfect credit scores—definite benefits for many Canadian small business borrowers. However, Mitelman said where the company really exceeds expectations is in user experience.

“We focus entirely on small business,” he said. “We understand the needs of small businesses and how they seek to borrow. We have built product and systems around this understanding. While borrowing as a small business has been hard traditionally, our approach radically simplifies it.”

If you’re a Canada-based small business in need of fast financing, learn more about Thinking Capital at www.thinkingcapital.ca. You can also check out their Knowledge Center for everything you need to know about small business funding.