Forty-one percent of small business owners lack a financial backup plan in case of emergency according to Reliant Funding’s recent Small Business Report. Among those who have a plan, 20 percent have $75,000 or less socked away, and 3 percent have no emergency savings at all.

RewardExpert spoke with the alternative finance company’s CEO and founder, Adam Stettner, about the dangers of financial unpreparedness and how Reliant Funding helps small business owners in need of working capital.

Solving a Common Small Business Challenge

Stettner started Reliant Funding in 2008 at the height of the worst financial crisis since the depression. Though he was a successful originator of student education loans, the banks he usually worked with began ignoring his phone calls. He realized that if he was having difficulty securing financing despite performing flawlessly as an originator, other small businesses must be struggling even more.

“This led me to research what it was like for a small business that needed to obtain financing and wanted to build a relationship with a source of capital,” Stettner explained. “That was the catalyst for my switch into serving small businesses.”

“Reliant Funding advocates for the growth and success of small business in America,” he continued. “We know that small businesses need money; it’s not a question of if, but of when. Because of that, we’re not just about providing capital but also about creating an ongoing relationship so the next time a need strikes, we are here for them.”

While Stettner’s company provides merchant cash advances, equipment financing, and small business loans to clients across a variety of industries, he said all of Reliant Funding’s clients have a few traits in common.

“They are entrepreneurial in spirit, work very hard, and have lots of people relying on them,” he noted. “Those traits are universal, and all of those things are pretty heavy responsibilities to carry.”

Construction and retail companies, restaurants and bars, transportation and auto repair businesses, and medical providers make up a large portion of Reliant Funding’s client base. But Stettner said any business that isn’t corporate owned or doing tens of millions of dollars in revenue can benefit from the company’s financing services.

“There are very few businesses that we don’t want to work with,” he continued. “We look for businesses that have regular cash flow. And the nice thing is that the majority of American small businesses do.”

A Trio of Financing Solutions

Merchant cash advances are Reliant Funding’s core product. Stettner described it as a hybrid of traditional financing and factoring.

“We advance money to a business and then, as they make sales in the future, they repay that advance,” he said. “We’re basically purchasing future sales. As the receivables come in, the business repays us.”

Because the financing is structured in this way, Stettner said that Reliant Funding is able to make advances without a personal guarantee, pledged assets, or collateral.

“Merchant cash advances don’t affect the business owner’s debt-to-income ratio or their ability to borrow elsewhere,” he continued. “We’ve funded hundreds of millions of dollars this way, and do it on our own balance sheet.”

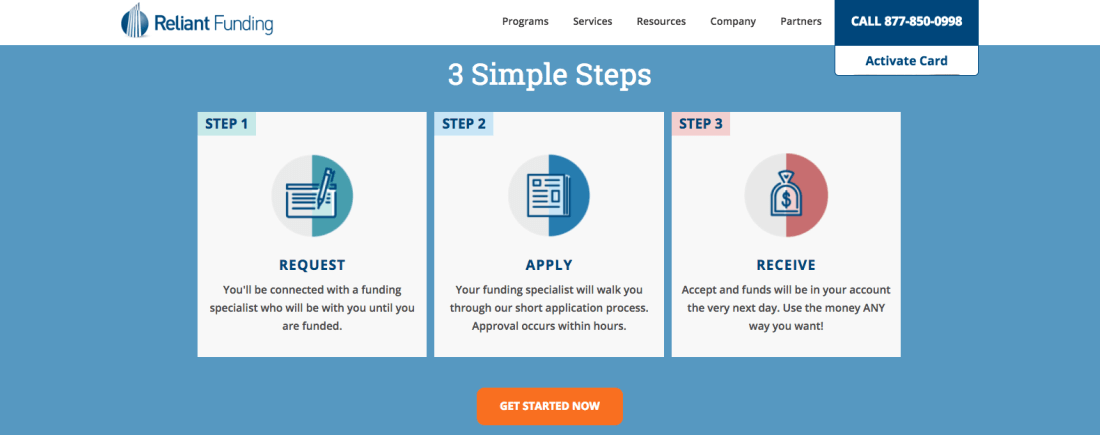

Reliant Funding approves over 70 percent of merchant cash advance requests, providing the business has been operating at least a year and has a minimum of $100,000 in annual revenues. A cash advance requires minimal paperwork and has no restrictions on how the money may be used. Approved small businesses can get $5,000 to $500,000 by the next day.

If a merchant cash advance isn’t the best solution for a particular small business, Reliant Funding also offers traditional small business loans.

“There’s a lot less flexibility with a business loan,” Stettner said, “but if a merchant cash advance isn’t the right product for a business, we want to make sure we have other products to offer. Working with us on a small business loan will be a lot less onerous than working with a traditional bank in the way of paperwork and time. We can turn a small business loan inside of two days, where a bank will typically take many weeks.”

For some small businesses, equipment leasing offers another financing option.

“If a business wants to buy a piece of equipment, they can use that equipment as collateral for the loan,” Stettner explained. “We’ll draw the financing out across the useful life of the equipment. That may offer payment and tax benefits beyond the other two types of products.”

Satisfying Immediate Financial Needs

While 9 percent of the small business owners surveyed by Reliant Funding for its Small Business Report had never heard of alternative finance, and 41 percent were familiar with the concept but had never used an alternative finance product, Stettner said that tools like merchant cash advances can be invaluable when emergency situations strike.

“When business owners have a need for capital, it’s usually an immediate need,” he said. “It’s often an opportunity that has come up and is time sensitive or a bill of some kind such as taxes or an unforeseen payroll situation. You can lose business if you’re not able to fund a project quickly. And you can lose employees if they feel like there’s a lack of stability in your organization.”

Because many small business owners are already personally fully vested in their companies, Stettner said they may think they’re out of options when they have a financial need.

“In reality, they aren’t,” he concluded. “The business may actually be the option. If it’s operating and making sales, whatever those sales are, that in itself, with a product like ours, can create access to capital and a funding relationship.”