Purchasing a new home is a very exciting time in one’s life, especially for first-time homeowners. It can also be a very stressful time since buying a home is one of the largest purchases you’ll make in your lifetime. It can be a monthslong process of credit checks, pre-approvals, document requirements, house shopping, and finally closing. So, what can be done to make it easier for the consumer?

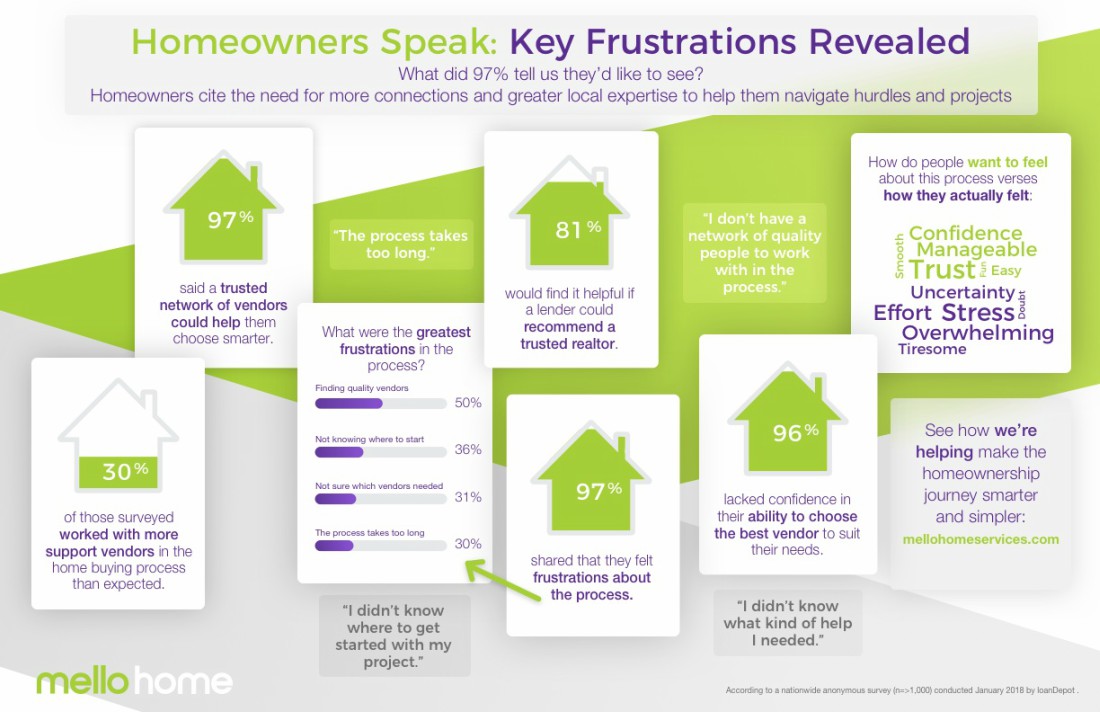

A recent study conducted by loanDepot and Drive Research found a whopping 97% of homeowners cited a need for more connections and greater local expertise to help them navigate the homeownership process. That’s the problem loanDepot hopes to solve with their new mello technology. We interviewed Julian Hebron, SVP of Corporate Affairs for loanDepot, to learn more about how they’re disrupting the home buying industry, while also improving the overall customer experience.

mello Technology Simplifies the Homeownership Lifecycle

loanDepot is an online lender that works by matching borrowers with the right loan option for their needs. In just eight short years, loanDepot is already the second largest nonbank consumer lender and the fifth largest retail mortgage originator in the U.S.

Hebron credits loanDepot’s ability to effectively scale their business through technology, training and effective management as major contributors to the company’s success. “We have a maniacal focus on the customer and make sure we are serving them as best as possible. We also match the best technology that we built ourselves rather than relying on off-the-shelf applications that we have to knit together,” Hebron said.

Last year loanDepot launched mello, a proprietary technology platform that allows home buyers to get their financing in order, from application to funding, on any device on their own, or alongside a local loan consultant who can advise and assist throughout the entire process. Last week loanDepot expanded upon the mello brand with the announcement of mello Home.

From house hunting, to financing, to closing, and even remodeling, mello Home will provide a seamless experience for the homebuyer in a unified brand experience, while also solving three common pain points.

-

Homeowners Want a Single Brand/Network

In the same survey, it was revealed that 97% of homeowners are frustrated working with multiple vendors during the homeownership process. When a consumer uses mello Home for the home buying process, they will be working with approved, reputable vendors, loan officers, and realtors, and be able to connect with them in one place instead of having to filter through reviews and connect with each vendor individually.

“What we’re trying to do is disrupt the entire homeownership lifecycle in a way that enables traditional players to still collaborate and work together,” he said. “The consumers entire homeownership lifecycle involves several vendors that are all complex and require local coverage in some way, except everybody starts online and eventually connects with a human,” he added.

This seamless connection of pairing recommended vendors with consumers creates a trusting environment that will ultimately lead to long-term success for both the homebuyer and the lender.

-

Start Online and Close Offline

There are profound stats supporting the fact that potential home buyers are starting the process online and then finishing the process offline with an actual human.

Once the customer receives pre-approval from mello Home, they can then be matched with a local, reputable realtor to help find their new home. All realtors on the mello platform are trusted by loanDepot’s local loan consultants and must conform to a set of service standards. mello Home’s service is free for consumers and real estate agents; however, agents will have to pay a fee for all closed transactions.

The home buying process has many steps, but the homeownership lifecycle doesn’t just end after you close on a new home. Some homeowners have plans to remodel immediately after purchase, while others plan to remodel later down the road. mello has a solution for that, too.

-

Increased Demand for Home Improvement

According to Zillow and the National Association of Homebuilders, the average homeowner spends $4,000 to $6,000 per year on repairs and upgrades, while more than half of homebuyers in 2016 purchased homes that needed improvements.

Later this year, mello will launch mello Home Improvement Services, which matches homebuyers with verified contractors. mello Home Improvement Services will serve two primary functions:

- Provide immediate approval of home improvement loans up to $75,000

- Allow contractors to offer financing at their own point-of-sale so financing is available in real time for the homeowner’s project

These home improvement loans are a little bit different than traditional home equity loans because they aren’t secured with property. Depending on the borrower profile, credit and loan amount, home improvement loans can be approved immediately to within a couple of days.

“The vision for the loanDepot mello brand family is to do for housing what Amazon has done for retail. Amazon started with books and a proprietary technology platform with great customer service. We started with mortgages on a proprietary platform and great customer service, and now mello Home is the starting point of moving into the rest of housing,” Hebron added.