2017 Holiday Spending and Credit Card Debt Survey

Most Americans begin the new year with a hangover, often both literally and figuratively. To begin the new year with a fresh face after the year-end holiday spending binge, it is imperative to effectively treat the financial hangover with which we awaken.

RewardExpert recently conducted a survey on holiday spending to determine precisely how much Americans borrowed and spent during the 2017 holiday season.

In our post-holiday survey of 620 Americans aged 18 and up conducted between January 8th and January 10th, 2018, RewardExpert found that consumers in America who engaged in holiday shopping spent an average of $1,059 on gifts, travel, accommodations, and other holiday-related expenses.

This figure represents a 5% increase over the average amount for the 2016 holiday season (modestly exceeding our in-house pre-holiday projection of an increase of up to 3.96%, extrapolated from monthly spending data from the Federal Reserve over a fifteen-year period).

While most Americans are starting the new year with substantial credit card balances that may take some time to zero out, young adults aged between 18 and 29 spent less and used credit least of all age groups, and have the lowest combined credit card balances.

For the rest of us, sometimes the best remedy is the hair of the dog method: with a little circumspection and more financial self-discipline, transferring high-interest credit card debt to a new balance transfer credit card can be an effective way to get your spring financial housecleaning done now.

Key Findings

Overall Holiday Spending

- Average holiday spending increased approximately 5.5% to $1,059 in 2017 over figures for the 2016 holiday season.

The overwhelming majority of Americans in all walks of life (76.94%) paid for their holiday shopping at least partially with credit.

- A total of 64.83% of respondents spent the same or more during the 2017 holiday season as they did in 2016, while only 7.1% reported spending less.

A surprisingly high 28.71% indicated that they did not spend any money on holiday-related expenses during the 2017 season.

2017 Holiday Spending

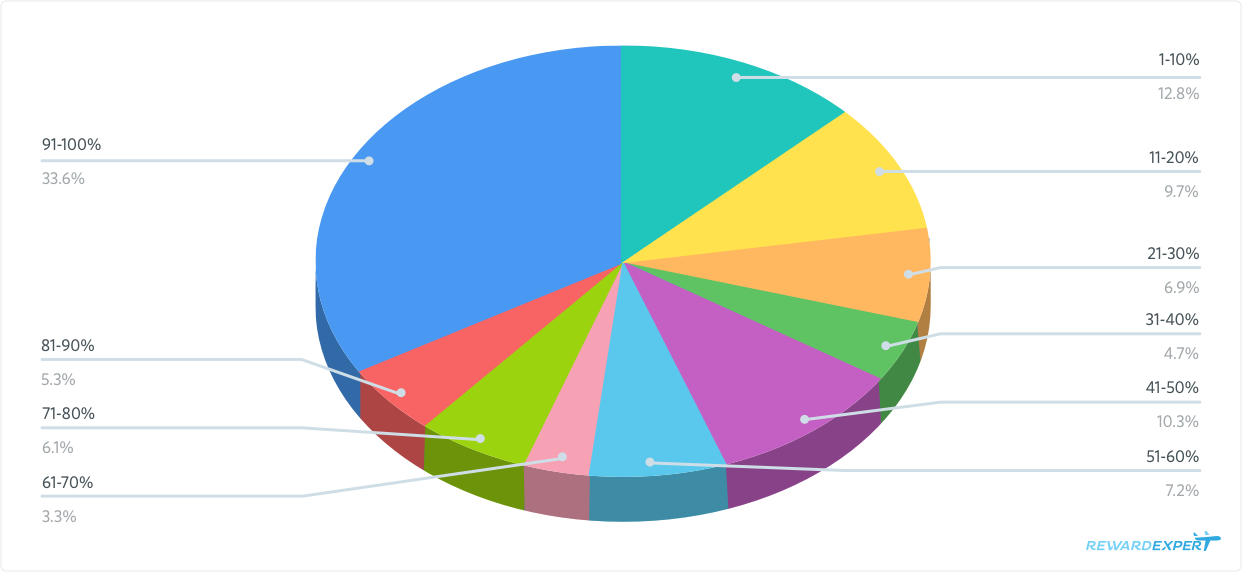

- Americans are starting off 2018 with an average combined balance of $4,528 on 3 credit cards, including bills racked up over the holidays plus other monthly expenses.

Generational Insights

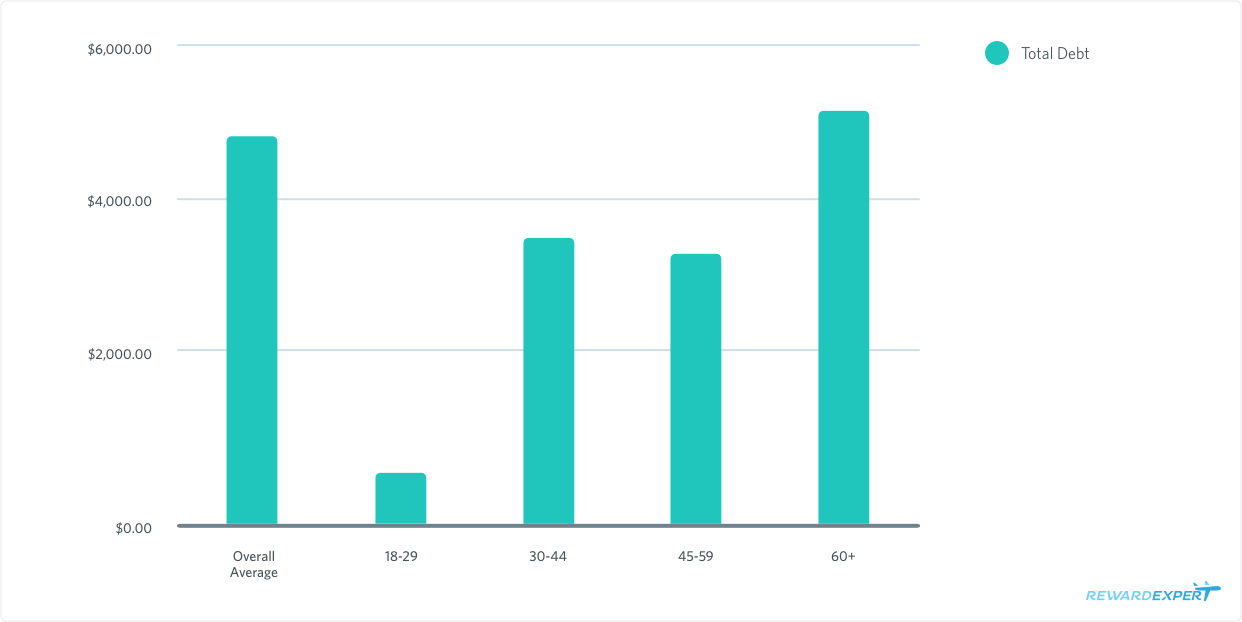

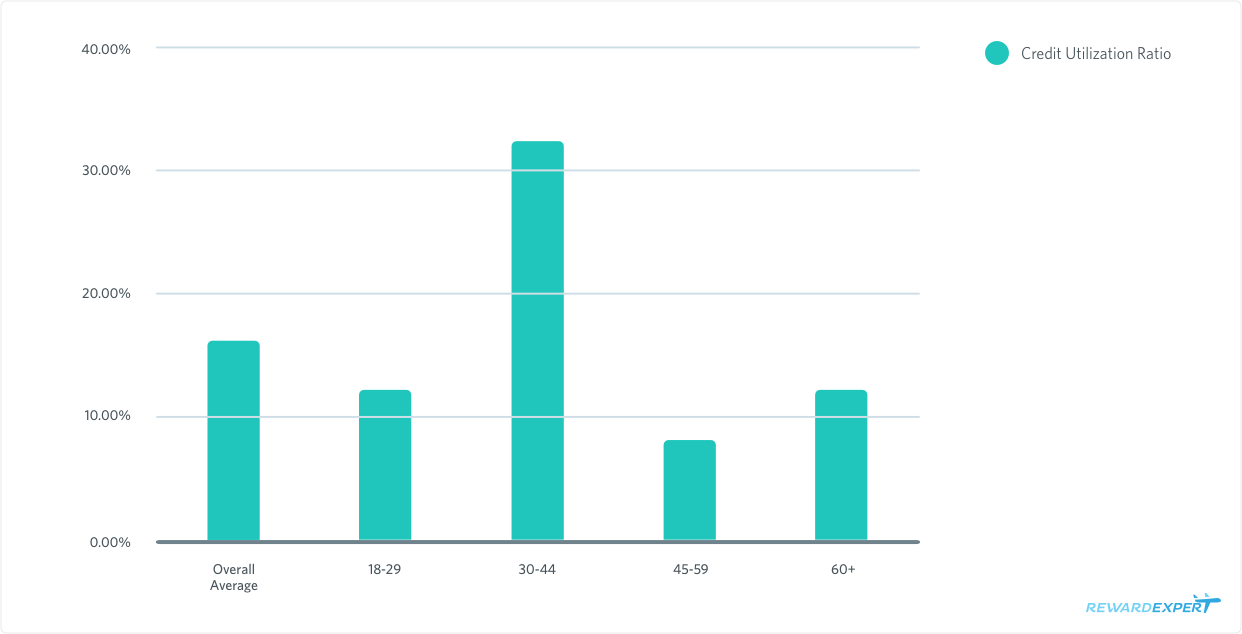

- Young Millennials are managing their holiday finances surprisingly well, almost as well as their parents’ generation. While holiday spending accounts for a whopping 76% of the outstanding credit card balances carried by 18-29 year olds, this is in part because the average balance in this cohort is so low ($549 out of $719 average balance). Credit utilization in this age group is only slightly higher than it is for Americans over the age of 45 (13.86% to 10.90%).

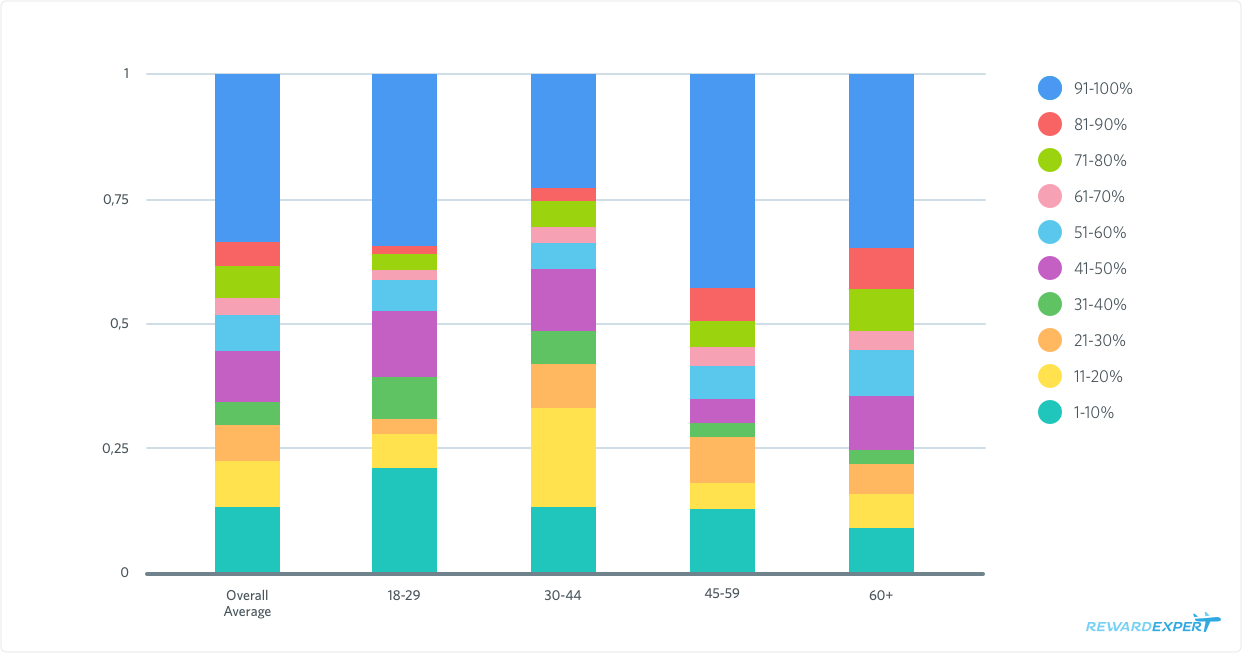

Combined Credit Card Balance

Credit Utilization by Age

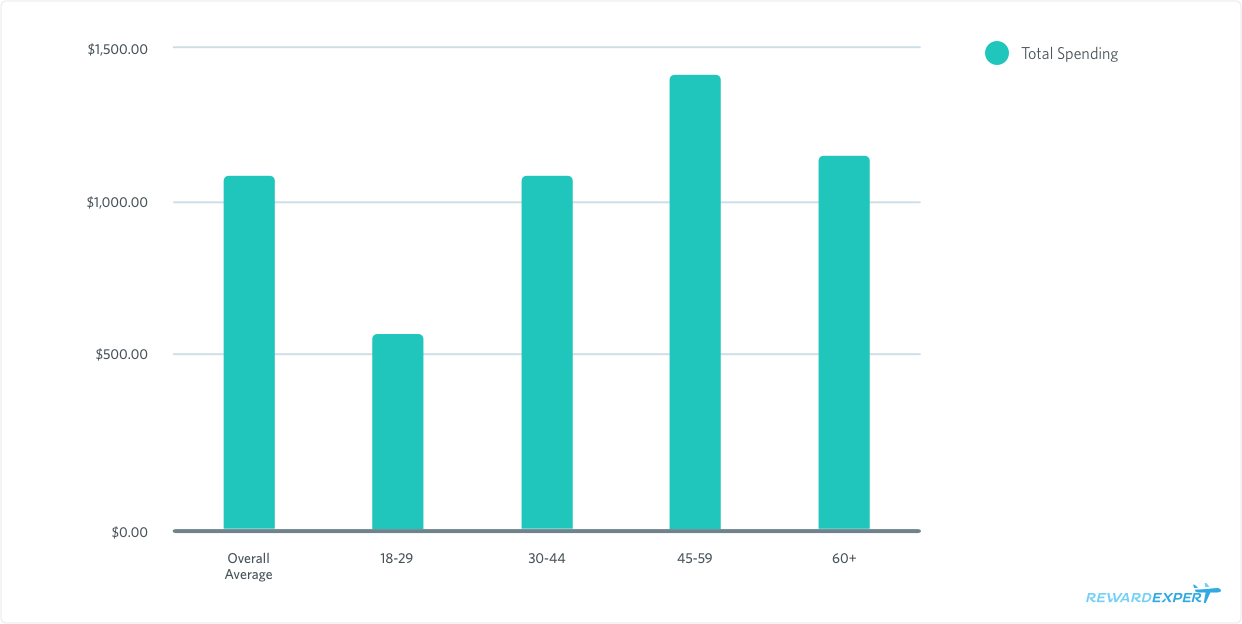

- Late Boomers/Early Gen Xers are the biggest holiday spenders, while young Millennials spend the least.

Americans aged 45-59 spent the most with $1,417 on average. The youngest end of our spectrum, participants aged 18-29, spent $549 on average. Interestingly, the next cohort up that straddles the Millennial and Gen X generations (ages 30-44), spent nearly twice as much as younger Millennials, averaging $1,090 in holiday expenses.

Holiday Spending by Age

- Young Millennials were least likely to have used credit cards to pay for holiday expenses, with 70.11% indicating that they had used credit cards for their holiday shopping, while Americans aged 45-59 were most likely to swipe their plastic at 89.53%. A surprisingly high number - over one third of all holiday spenders - put all of their charges on credit cards.

Percentage of Holiday Purchases Made With Credit Cards by Age

Overall Average Percentage of Holiday Spending on Credit Cards

- Older Millennials/younger Gen Xers are more pessimistic (or realistic) about paying off credit card debt quickly, with 43.48% expecting it to take longer than a month to pay for their holiday spending. Americans older than 60 were slightly more likely to plan on carrying a balance, with 44.19%.

Debt Management

- Americans who paid entirely with plastic added up to 53% to their balances over the holidays.

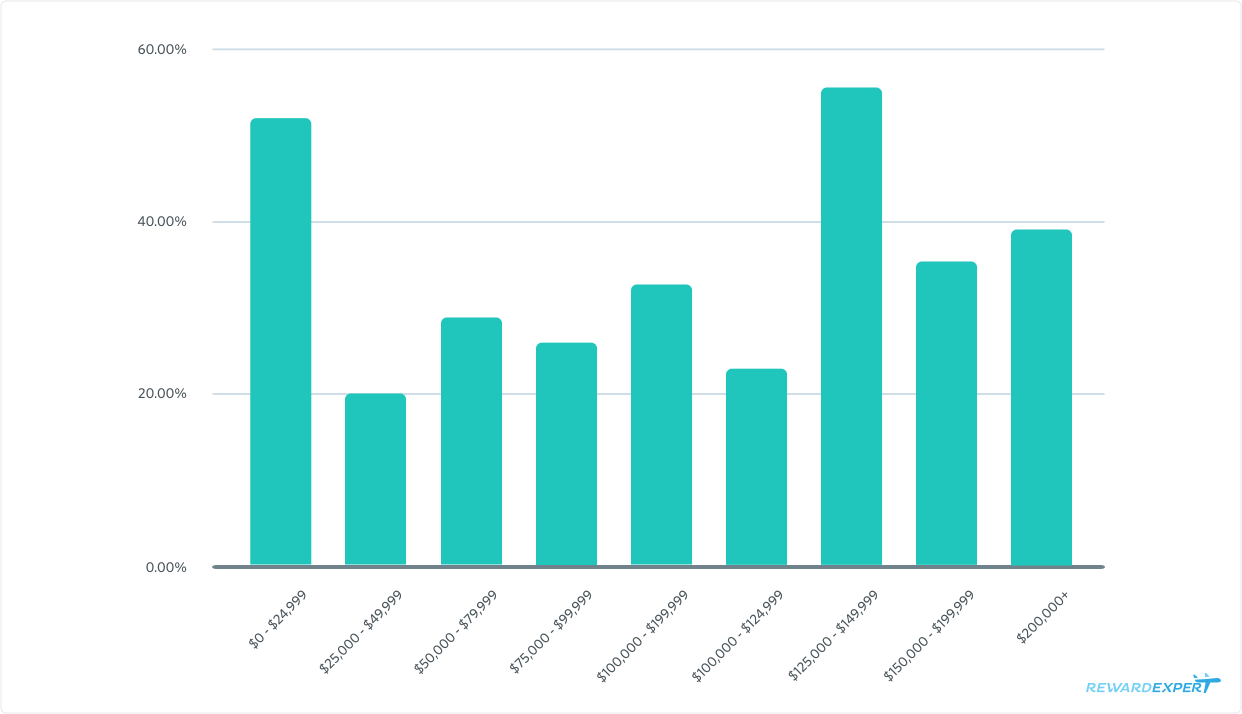

This figure was highest among high-income households, with holiday spending totals amounting to 52.26% of the average total credit card debt for respondents with annual household incomes between $125,000-$149,999.

Percentage Added to Credit Card Debt by Holiday Spending

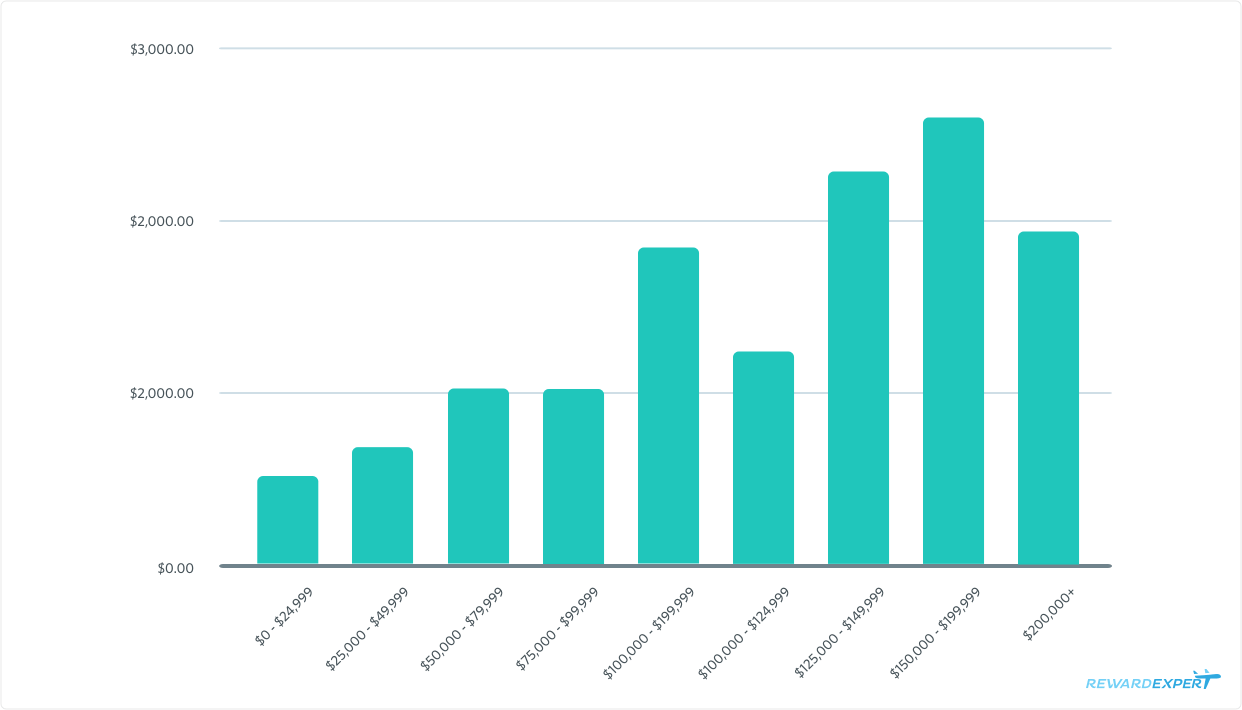

Holiday Spending by Income Bracket

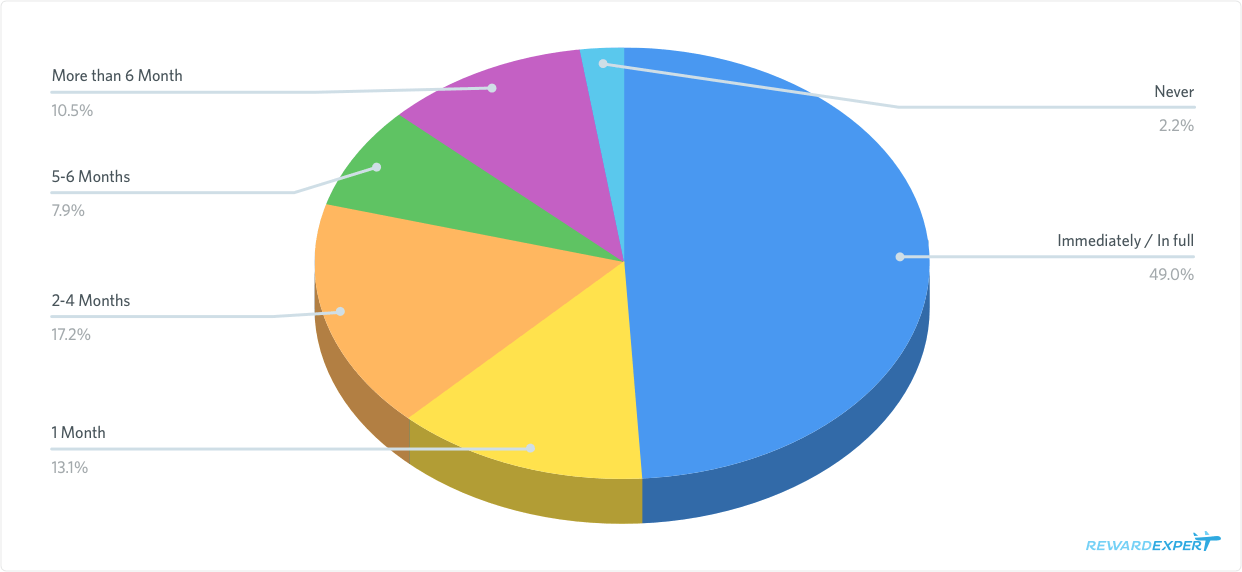

- More than half of those surveyed expected to pay off credit card balances resulting from holiday spending immediately, or in one month.

Only 10.68% expected or were willing to admit that they would expect to take six months or longer to pay off the balance accumulated over the holidays.

How Long to Pay Holiday Credit Card Bill

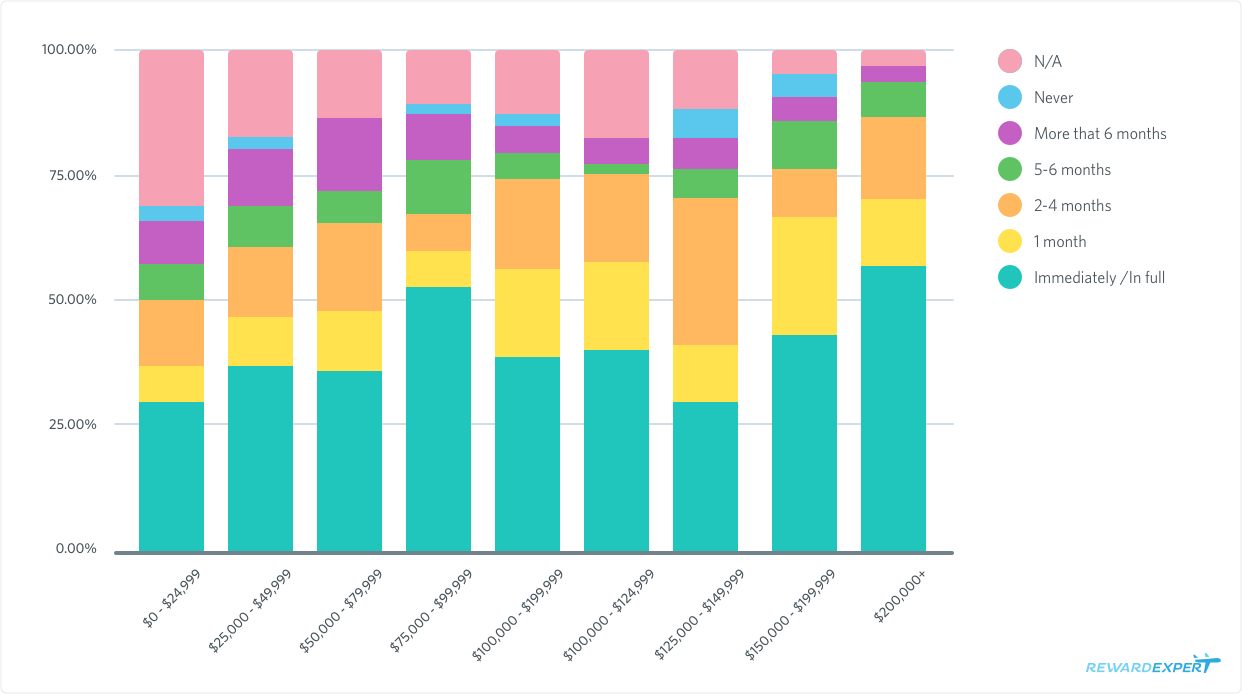

- Surprisingly, high-earning consumers are most likely to need more than a month to pay their January credit card statement.

Respondents with household incomes between $125,000 and $149,999 anticipate needing two to four months to pay of the bill they racked up over the holidays. For those staring down payoff periods longer than one month, it would be wise to consider applying for a credit card geared toward balance transfers in order to reduce or avoid interest charges.

Length of Time to Pay Holiday Credit Card Bills by Income

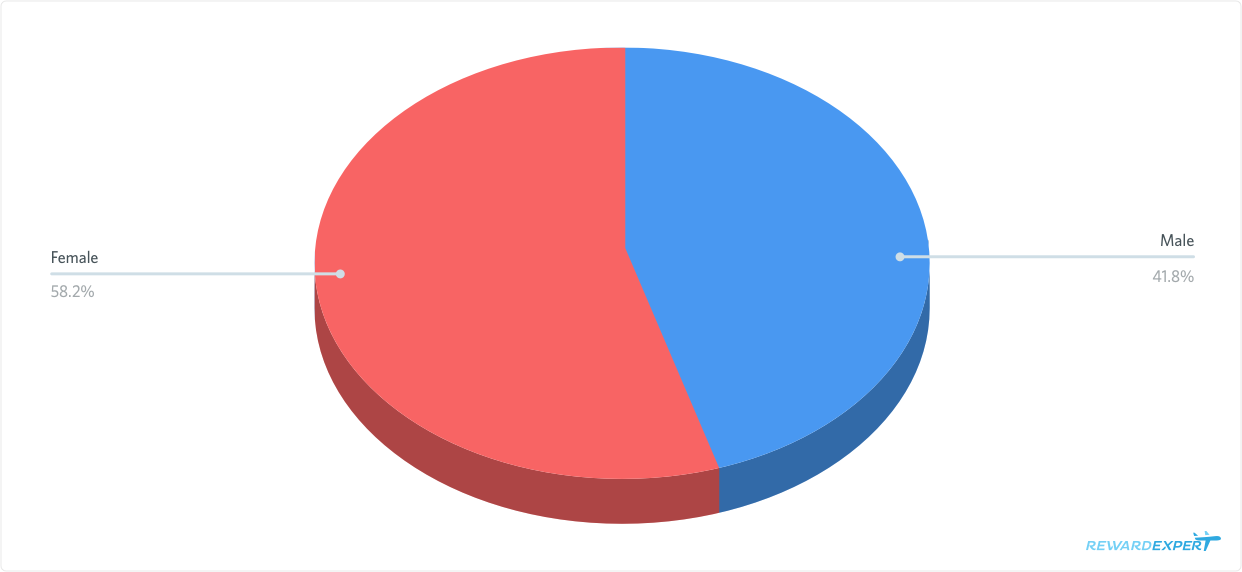

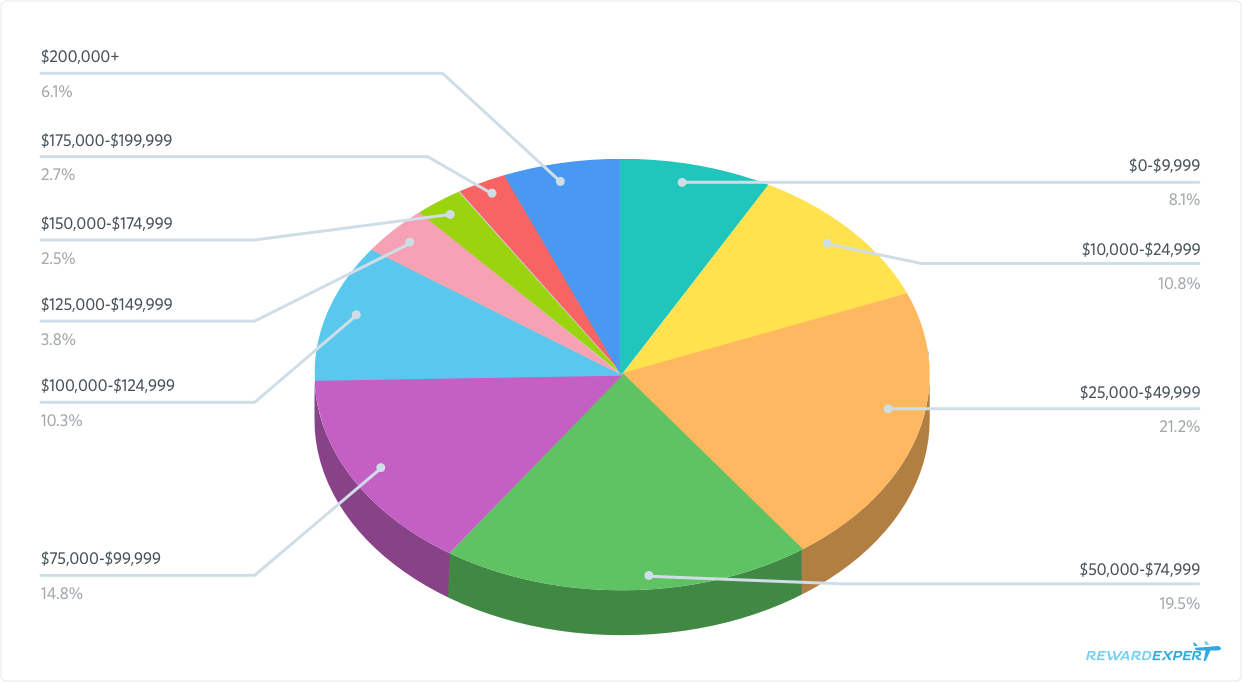

Survey Demographics

Gender Breakdown

Income Breakdown

Methodology

RewardExpert surveyed 620 Americans aged 18 and older Survey was conducted January 8th through January 10th online through SurveyMonkey Audience. Margin of Error +-4% for all responses. 112 respondents between ages 18-29, 149 respondents between ages 30-44, 145 respondents between ages 45-59, and 360 respondents ages 60+, margins of error are +- 9%, +-8%, +-8%, and +-5% respectively. The survey had 443 respondents with holiday expenses and at least one credit card who answered all survey questions. Margin of error for this sample is +-5%. Survey sample was subject to demographic balancing, but as an online survey it may not represent the general population at large. Averages calculated for full sample, qualified subset, and each age group.

Indicators

Sources: